Naked Puts (Part 9)

Posted by Mark on December 22, 2015 at 06:39 | Last modified: November 7, 2015 12:58I suspect my discussion about leverage is as important a concept to explicate as anything else regarding this approach.

I started by comparing naked puts and long shares with equal capital risk. The graph makes it clear that long shares are more profitable. To get that profit, though, I was going to have to endure a whole lot of pain.

This process also helped me realize the trade can be very expensive in terms of capital risk. With options it looks possible that I can take on even more capital risk and still be safer (historical drawdowns) in bear market conditions.

As a cautionary note, I feel people must understand other details I did not cover before trading this strategy. I did not take several more blog posts to explain technicalities I work with every day. One should understand differences between underlying markets, what options to trade, and when to trade them. One should also understand details about execution and about transaction fees. I took all this into account when running the numbers.

Specific details will also vary from one trader to another in terms of position sizing. One needs to understand what kind of accounts will allow this type of trade. One needs to understand margining and what to expect as the market moves. Fixed vs. variable position sizing should be understood along with particular implications about the graphs as I have presented them. These are things people learn as they take time to study how options work and how to trade them. Many of these details I have described elsewhere in this blog.

I may come back at a later time and flush out more of the technical details. For now though, I will affix the bow: that’s a wrap!

Categories: Backtesting | Comments (0) | PermalinkNaked Puts (Part 8)

Posted by Mark on December 10, 2015 at 05:38 | Last modified: November 5, 2015 07:15I want to go in another direction today and consider exactly how I might go about doing the naked put trade, which really becomes a question about position size.

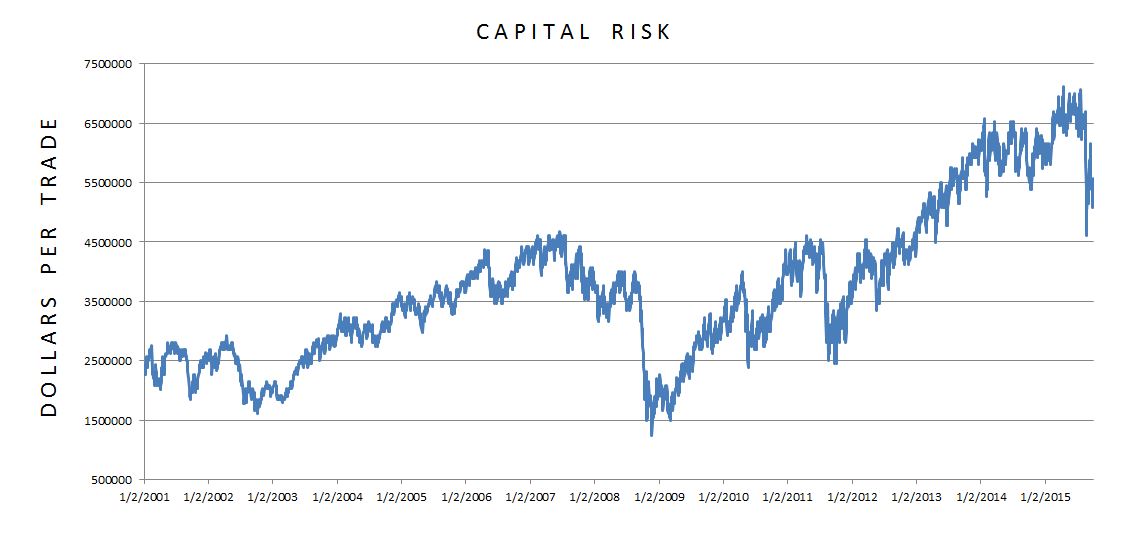

As I prepared the initial graph comparing naked puts with long shares, I became aware how much capital risk this arbitrary position size was commanding:

The graph illustrates two important points:

(1) This is not a constant capital-risk trade

(2) Capital risk is extremely large.

With regard to backtesting, (1) is very important. Position sizing should be held constant throughout the system development process. This allows for an apples-to-apples comparison of PnL changes throughout the period of study. A drawdown (DD) at any point should be evaluated as if it occurred from Day 1; this is one way of interpreting maximum risk.

Even though capital risk did not remain constant, contract size did and for that reason I believe the backtest is acceptable. I had a gross dollar target range for profit and maximum loss that remained constant regardless of underlying price. Leverage, being directly proportional to capital risk, is what changes. This is a difficult concept to understand.

With regard to (2), it especially became evident how large capital risk is when I realized the graph shows one trade at a time. With an average of 27.6 days in trade, I can multiply the average capital risk by 27.6 to get an estimate of how much capital risk is on at any given time. Over the 14+ years that number is $103M each day!

To personalize this trade, clearly I have to cut down the position size and then make some decisions about whether the return potential vs. expected DD is acceptable for me.

Categories: Backtesting | Comments (3) | PermalinkNaked Puts (Part 7)

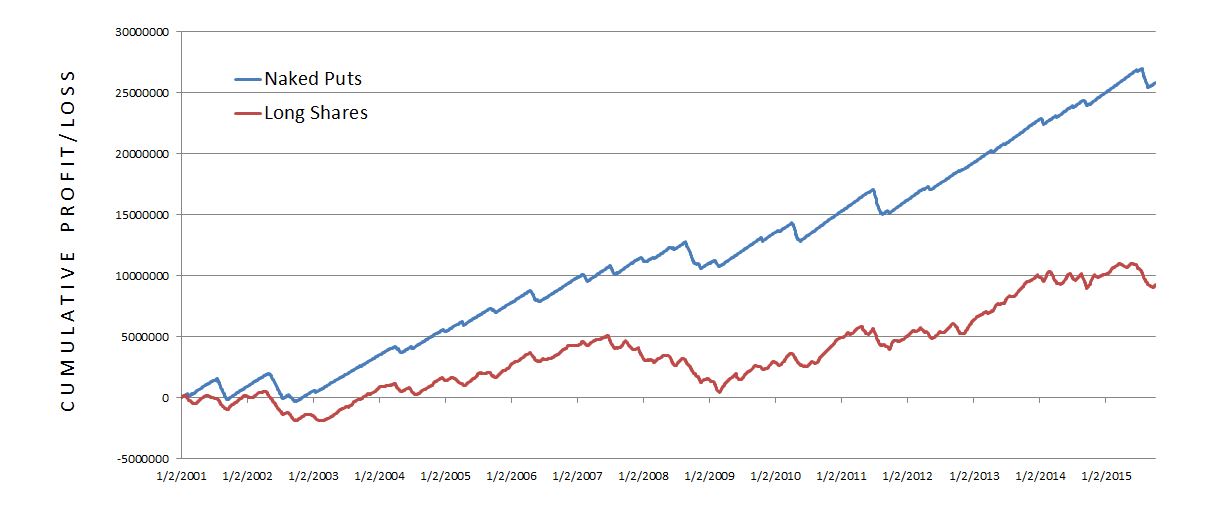

Posted by Mark on December 7, 2015 at 05:16 | Last modified: November 5, 2015 06:51Comparing long shares and naked puts with equal capital risk ended up being far superior for the latter in terms of drawdown (DD).

If I cut the long shares position size by a factor of eight, here is how the two compare:

This is a huge difference. The long shares now gain $9.31M (down from $74.5M) compared to the (same) $25.8M for the naked put trade. In other words, observation 1 has been reversed. The naked put trade still has a lower max DD (-$2.27M vs. -$4.65M). The naked put trade still has better consistency with an average (mean) daily DD of -$378K (vs. -$924K). The naked put trade is still in DD only ~49% of the time (vs. ~82%).

The naked put trade appears to make more money with greater consistency than long shares.

For me, putting context around this trade means playing devil’s advocate over and over again. This trade certainly looks pretty good. What am I missing?

Particularly impressive to me is the fact that even with 8x as much capital risk, the option trade has less DD risk.

But it does now have eight times as much capital risk. Were the market to take a huge hit, the option trade could lose much more than the long shares.

In deciding whether to do this trade, I think one’s level of pessimism must be assessed. The “huge hit” that would cause the naked put trade to lose more than long shares would have to be worse than what we’ve seen since 2001. So if you are truly the prophet of doom, you worry about a catastrophe worse than the Flash Crash (2010), than the August 2015 correction, than September 11 (2001)… you worry about a decline worse than the 2008 financial crisis.

Depending on your exact level of paranoia, at some point I would wonder why you are even in the market at all. Keeping your money safe under the mattress might be a better choice.

Alternatively, maybe you simply follow the same traditional recommendation given for long shares: allocate a limited percentage of the portfolio to naked puts.

Categories: Backtesting | Comments (0) | PermalinkNaked Puts (Part 6)

Posted by Mark on December 3, 2015 at 06:24 | Last modified: November 5, 2015 06:55The third observation I made in comparing performance identified much greater consistency with the naked puts than the long shares trade.

The greater consistency can be seen in terms of the straight blue line that moves in a narrow range relative to the jagged red line that moves in a wide range.

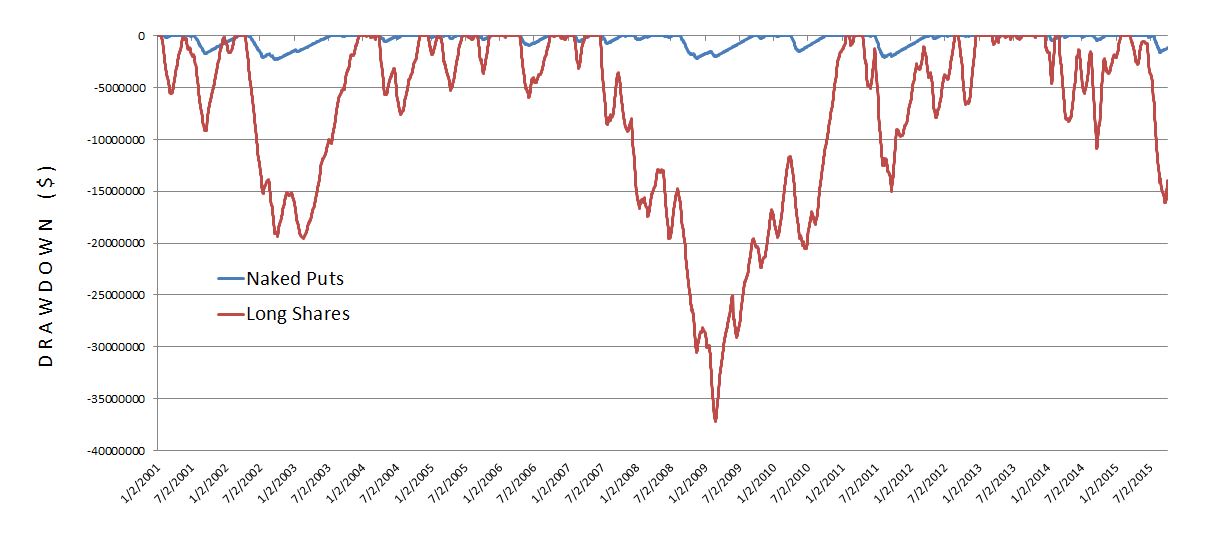

An even better illustration of this is seen in the drawdown (DD) graph. The blue line spends most of its time near the top ($0) whereas the red line does not. More specifically, the long shares are in DD for 3033 trading days (~82% of the time) vs. 1827 trading days (~49% of the time) for the naked put trade.

Psychologically, “days in DD” is a very important measure of trade consistency and how likely I am to stick with the strategy. When in DD I feel something between “slightly annoyed” or “not overly happy” to despondent, angry, sleep-deprived, and freaking out. The excruciating psychic pain that forces me to cash out at catastrophic loss happens while in DD. When not in DD, my account equity is reaching new highs. These are times I feel happy and on top of the world.

To better understand the naked put trade, I started out with an apples-to-apples comparison based on capital risk. Clearly while capital risk is the same, risk in terms of DD over the years is not. Once I determine my risk tolerance, capital allocation to the long shares would have to be much smaller than for the naked put trade to equalize the DD.

Put another way, for comparable levels of DD I am able to do the option trade in greater size than the long shares. This is not a surprise when we think about options in terms of leverage. What I find ironic is that people often say options are excessively risky because of their leverage. Here it becomes clear that only by increasing the option leverage can we get comparable risk, which completely flies in the face of “common wisdom.”

Categories: Backtesting | Comments (3) | PermalinkNaked Puts (Part 5)

Posted by Mark on November 30, 2015 at 06:21 | Last modified: November 5, 2015 06:57I left off with a graphical performance comparison between the long shares and naked put trades.

Aside from being a yardstick for starting equity required to do a trade, drawdown (DD) may also be understood in terms of risk tolerance. If I run a backtest and find a max DD of -$200,000 then I need to ask myself whether I would feel comfortable continuing to trade a strategy that had lost $200,000. Human nature is actually to overestimate risk tolerance since it’s easy to imagine how I might handle a particular loss but much more difficult to tough it out when I’m in the middle of it. Combine this with that trader’s adage “your worst DD is always ahead of you” and the number used to evaluate risk tolerance should be higher than the max DD.

To summarize, I have now discussed two ways of evaluating max DD: as a measure for starting equity and as a measure for risk tolerance. The biggest concern with insufficient starting equity is that I may go bust. In my opinion, though, the biggest risk for a trading strategy is not necessarily that it will bankrupt me. Rather, it is that I will lose enough money to get scared, to lose sleep, to be constantly worried, and other related feelings that will eventually force me to cash out at the absolute worst time possible to alleviate the psychic pain.

Here is a graph of DD for the naked put and long shares trade:

Clearly the long shares trade is far more risky than the naked put trade. The max DD is $37.2M for the long shares and $2.27M for the naked puts. On any given day, the long shares can be expected (arithmetic mean) to be in a $7.4M DD compared to $378K for the naked puts: a 19-fold difference! As a result, I would want to trade the long shares in much smaller size than I would the naked put trade and that would decrease the estimated profit I could expect from it.

Categories: Backtesting | Comments (1) | PermalinkNaked Puts (Part 4)

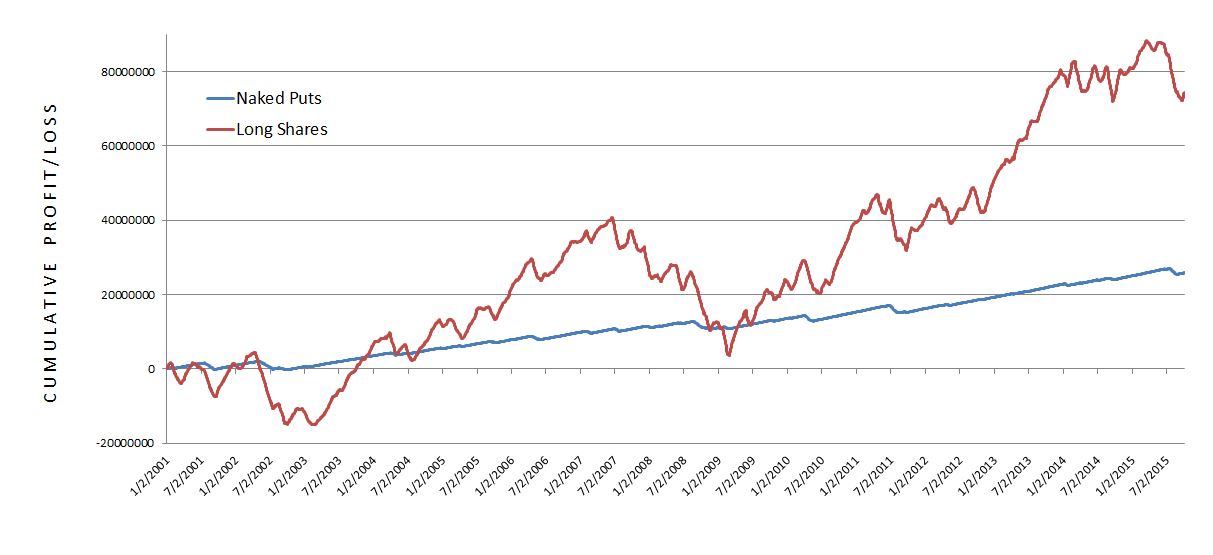

Posted by Mark on November 25, 2015 at 06:27 | Last modified: November 5, 2015 06:58In order to better understand the naked put trade, I have designed an apples-to-apples comparison between the naked put and long shares trade.

Here are the results:

Three main observations jump out at me and I will discuss these in order:

- The shares trade is more profitable

- Drawdown in shares trade is much worse

- Naked puts are much more consistent

First, the shares trade is more profitable. No doubt about that! The shares gained $74.5M compared to $25.8M for the naked puts over 14+ years. Before I get starry eyed in thinking how I will do the shares trade and make sooooo much money, though, I need to better understand how much I can lose and how much I need to start the trade.

The latter detail is also addressed by 2 above: the drawdown (DD) in the long shares is much worse than the naked put trade. DD is the peak-to-trough decline during a specific period of an investment or trade. DD represents a minimum starting equity amount to do a trade. If the worst (maximum) DD ever seen over the period of a backtest is -$200,000 then I better have at least $200,000 in the account to do a trade. If I don’t then I’m at increased risk of going bust. Traders often say “your worst DD is always ahead of you” to suggest no matter what size DD you found in backtesting, a larger DD can be expected to occur in the future. To be safe, then, my starting equity should be greater than max DD.

DD is also important with regard to risk tolerance. I will pick up here next time.

Categories: Backtesting | Comments (3) | PermalinkNaked Puts (Part 3)

Posted by Mark on November 24, 2015 at 07:00 | Last modified: November 3, 2015 07:03I found some encouraging initial results with regard to the naked put trade but I still need more context to understand what that means and what I can reasonably expect from the strategy.

Prospective investors often want to know if a particular strategy beats its “benchmark.” In order to assess this, I will do an apples-to-apples comparison between naked puts and long shares by equalizing capital risk.

Capital risk for a naked put trade is roughly the strike price minus credit received multiplied by the number of contracts multiplied by 100. For each trade I get a trade gain/loss along with start/ending dates.

For the corresponding shares trade I took the naked put risk divided by underlying price at trade inception to get the number of shares purchased. I then multiplied this by the change in underlying price between the start/ending dates above to get the corresponding trade gain/loss.

As an example, suppose I sell 20 naked puts on XYZ stock, which is currently trading at $100/share. The strike price is $90 and I collect $2.00 per contract. If I get assigned then I have to pay $90/share but I collected $2/share up front. My total risk is therefore:

($90/share – $2/share) * 20 contracts * 100 shares/contract = $176,000.

If you’re into unit analysis, this is:

$/share * contracts * shares/contract = $

“Share” and “contract” mathematically cancel out.

For $176,000, I could buy $176,000 / $100/share = 1,760 shares. The corresponding profit/loss on the shares would then be the price change of XYZ during the trade multiplied by 1,760 shares.

The maximum potential profit on the naked puts would be $2.00/share * 20 contracts * 100 shares/contract = $4,000.

I will show results next time.

Categories: Backtesting | Comments (1) | PermalinkNaked Puts (Part 2)

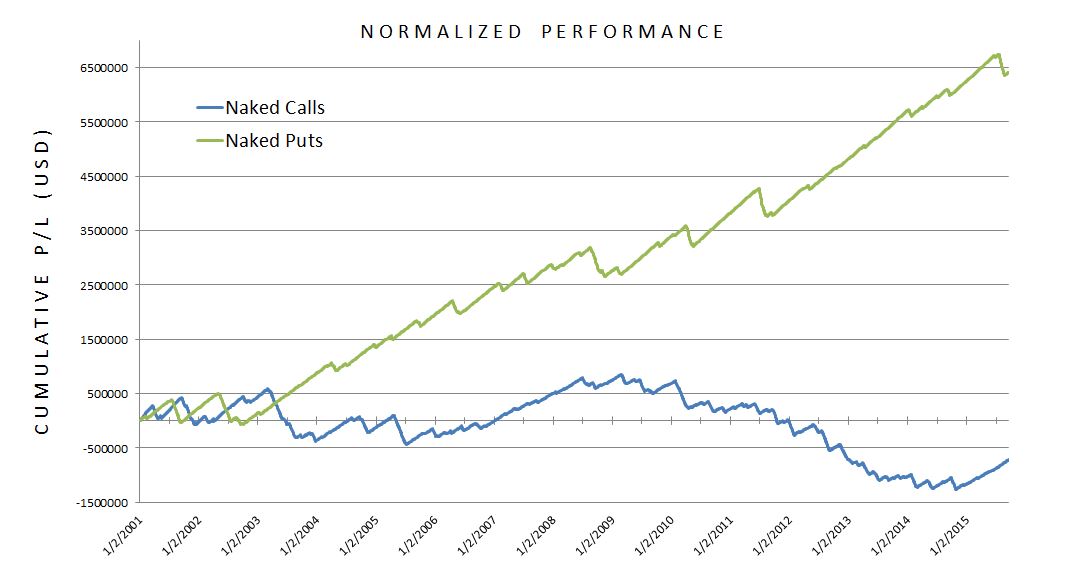

Posted by Mark on November 23, 2015 at 07:27 | Last modified: October 31, 2015 14:28In my effort to put more context behind the trade, I found something dramatically different with naked puts than I did with naked calls.

As previously discussed, I’m trying to understand whether the trade offers an edge. Putting context behind a trade is an attempt to better understand what I can reasonably expect in terms of critical trade parameters like profit/loss, drawdown, and total risk.

Below is a graph of cumulative profit/loss across all trades from 1/2/01 through 9/18/15:

Normalized performance means I adjusted numbers for position size difference.

As an initial impression, I would not want to do the naked calls. Period. In following along that blue line, I see no reason to hold out any hope for consistent, long-term profitability.

The naked puts are a totally different story. The green line is, for the most part, beautiful and pretty much what I would expect for a bullish trade. If I highlight the market corrections:

Now we can clearly see [circled] September 11 (2001), the market downturn of 2002, the 2008 financial crisis, the Flash Crash (5/10/10), summer 2011, October 2014 (small), and the recent correction this past August.

The naked call trade is flat to lower with the market mostly up over the last 14+ years. I did expect to at least see profitability there, though, because of the margin of safety the trade affords.

The naked put equity curve, on another hand, seems amazingly resilient. I’m not happy with the first two years but that is to be expected from a bullish trade in a bear market.

So what does all this mean? Is there edge? Do I know yet? What context is still missing?

One thing that would help is comparison to a benchmark. I will move in that direction next time.

Categories: Backtesting | Comments (1) | PermalinkNaked Puts (Part 1)

Posted by Mark on November 20, 2015 at 06:18 | Last modified: October 31, 2015 14:28Like I did for naked calls, today I will start to analyze my data on naked puts.

As an aside, I listened to a podcast this morning by a guy who supposedly trades for a living. He argued most traders fail because they cannot define their trading edge. He emphasized discretionary traders at one point because they are notorious for not having statistics to back their methodology.

I agree with that because usually with discretionary trading, parameters are not the same from one trade to the next. A set of guidelines might have a range over which action should be taken. An infinite number of possible trades may result depending on where action is ultimately taken and “gut instinct” is usually the deciding factor.

The goal of this post is to put some context around naked puts and try to determine whether they provide an edge.

I backtested from January 2, 2001, through October 2, 2015: 3,695 trades total.

87.8% trades (3,253) won.

12.2% trades (452) lost.

Mean days in trade was 27.6 with a standard deviation of 10.6.

Mean profit on 2,760 trades was $14,585 with a standard deviation of $1,929.

Mean days in winning trade was 29.7 with a standard deviation of 9.45.

Mean loss on 452 trades was $47,833 with a standard deviation of $17,551.

Mean days in losing trade was 17.1 with a standard deviation of 10.9.

Average trade: $6,970

Average annual profit: $92,257

Profit factor: 2.19

Really?

The relative magnitude of most of these dollar amounts is not so important. I backtested this with a position size four times larger than that of the naked calls.

One system statistic that I think speaks volumes is the 2.19. This is definitely worthy of a second look.

Categories: Backtesting | Comments (0) | PermalinkBacktesting Methodology (Part 2)

Posted by Mark on November 17, 2015 at 05:46 | Last modified: October 31, 2015 14:24A common approach to option backtesting often falls prey to insufficient sample size. The second big problem I see with most backtesting is potential invalidation by serendipity.

Yes serendipity, which is defined as “the occurrence and development of events by chance in a happy or beneficial way.”

Consider the following example. Suppose someone backtests a strategy over the last 10 years and starts each trade with 45 days to expiration (DTE). This would be a typical monthly trade similar to the naked calls strategy, which averaged 24.39 days/trade.

If the backtesting looks good then s/he is excited (a la “happy or beneficial way,” above) because s/he has encouraging results after studying 10 whole years!

Is it conceivable that if they started the trade with 44 DTE then the results might not look so good? Yes. It’s also possible the results might look downright ugly.

What if they started the trade with 46, 43, or 47 DTE? What about 40 DTE? 50 DTE?

People have tried to claim that certain days are the best/worst to trade and I suspect nothing is farther from the truth. Until I see such a claim statistically validated, I will consider all days to be equivalent. On a historical stock chart they all reduce to bars or candles. A study that performs well on 45 DTE better look good across a range of possible starting dates. If it doesn’t then go ahead and trade it with your money but I certainly will not be gambling with mine.

Put another way, if the other days aren’t looked at or included then I don’t think the backtesting amounts to a hill of beans. They should all be similar and if results look good on some days and bad on others then maybe the encouraging ones are simply due to chance.

This is why I backtested from 2001 through 2015 inclusive for a sample size approaching 3,700. I based my conclusions not on a particular starting date but on the average of all trades taken together.

Categories: Backtesting | Comments (0) | Permalink