Investing in T-bills (Part 4)

Posted by Mark on February 16, 2024 at 10:18 | Last modified: March 19, 2024 12:14I discussed put selling (also known as “short puts” or “naked puts”) last time as a way to participate in underlying stock appreciation in combination with T-bill investing. Before moving forward, I want to tie up some loose ends and present a different way of visualizing previous concepts.

Risk graphs are a way of visualizing potential risk and reward of option positions. I compared and contrasted such details for long calls and short puts in Part 3.

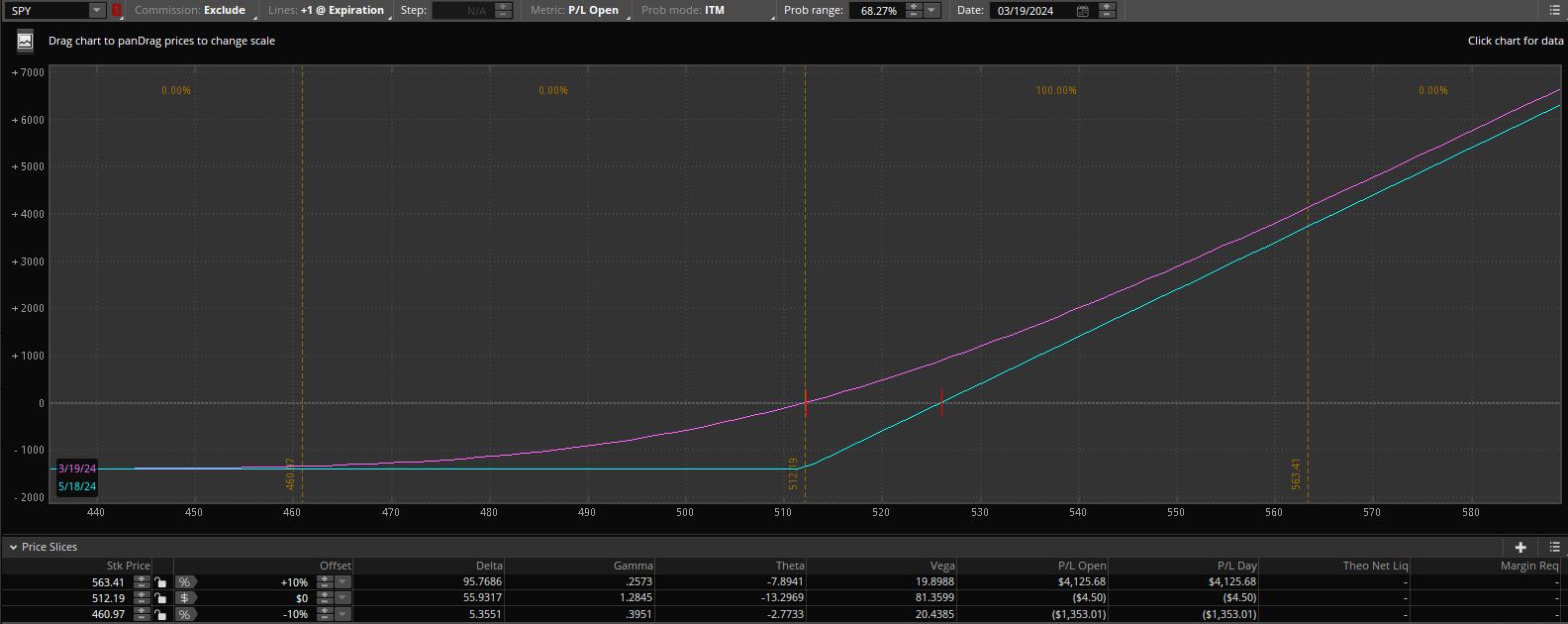

Here is the risk graph for a long call:

- This call is purchased for $14.14/share (the default multiplier for equity options is 100 shares per contract so buying one of these actually costs $14.14 * 100 = $1,414) with SPY [stock, or more precisely ETF] at $512.20/share (early morning on 3/19/24; see second-to-last paragraph here if the dates really confuse you).

- The purple (cyan) curve shows profit and loss today (in 59 days at May expiration) based on a range of prices for SPY.

- Note how the purple curve will sink down to the cyan over time. This represents the premium paid for the call and how some of that premium may be recovered by selling to close prior to expiration (total premium is reflected in the value of the cyan curve to the left: -$1,414).

- Note the unlimited profit potential as the curves have positive slope to the right.

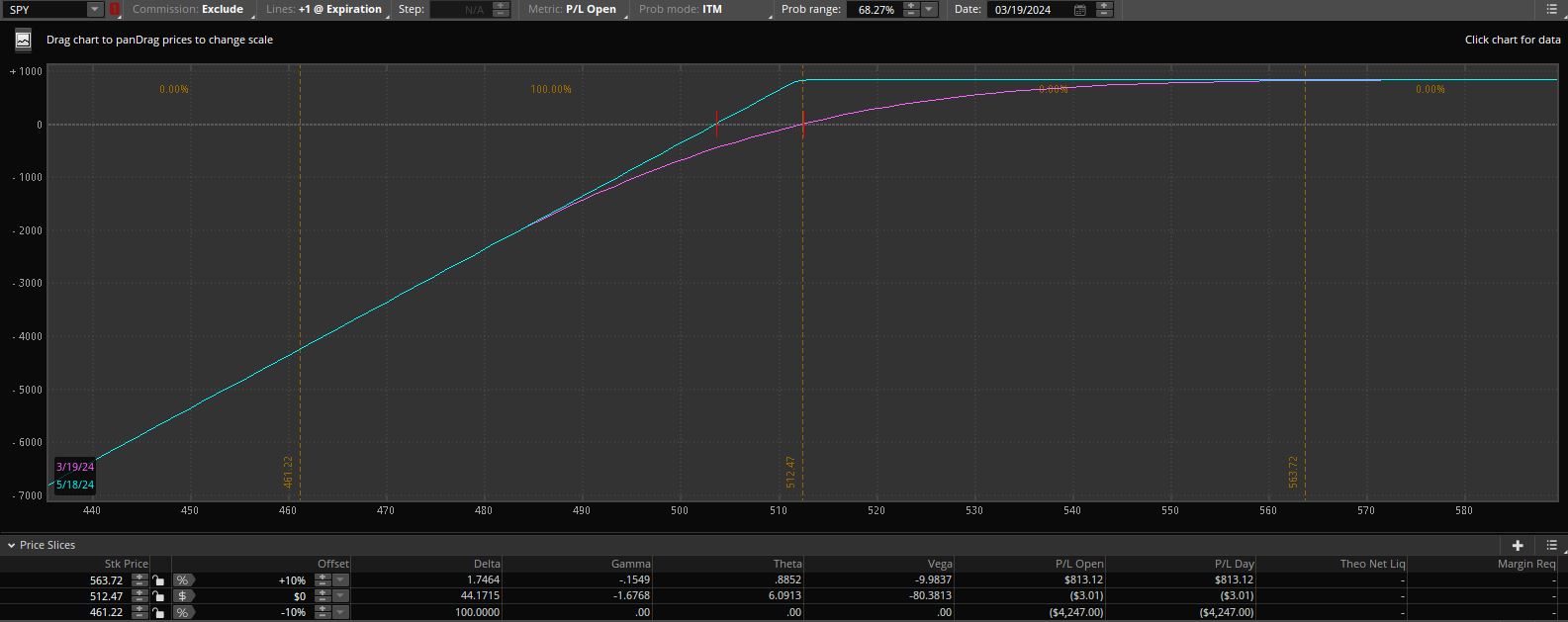

Here is the risk graph for a short put:

- This put is sold for $8.31/share ($831/contract) with SPY at $512.40/share (early morning on 3/19/24).*

- The purple (cyan) curve shows profit and loss today (in 59 days at May expiration) based on a range of prices for SPY.

- Note how the purple curve rises to the cyan over time. This represents the premium received for the put and how some of that premium must be surrendered when buying to close prior to expiration (total premium is reflected in the value of the cyan curve to the right: +$831).

- Note the unlimited [technically limited by SPY reaching zero because stock prices cannot go negative] loss potential as the curves have negative slope to the left.**

Buying calls depletes whereas selling puts raises cash that may be used to invest in T-bills. If the calls become profitable, however, then selling them will increase cash balance whereas closing a short put (or letting it expire) after the underlying stock has decreased can lower cash balance (more on this later).

I will continue next time.

* — The call is more expensive than the put because it includes over $2.00 intrinsic value. This is touched upon in

the third paragraph here, but I would refer you to an introductory book/article on options for a more complete

explanation. For at-the-money equity options, puts [premium] are generally more expensive than calls.

** — One naked put carries less risk than 100 shares of stock because its maximal loss is offset by the premium

received for selling it. This is discussed in further depth here.

Investing in T-bills (Part 3)

Posted by Mark on February 13, 2024 at 11:09 | Last modified: March 18, 2024 16:33In Part 2, I wrote about investing in T-bills while buying calls (also known as “long calls”) in the same account. Today, I will review that discussion and introduce put selling (also known as “short puts” or “naked puts”).

Long calls generally increase in value with the underlying stock once the increase is enough to offset the initial premium previously described as “rent.” In that example from the sixth paragraph here), I pay $13.73/share premium to buy the calls. After 62 days, my position will be profitable if SPY stock [an ETF] has gone up more than $13.73/share and no limit exists to how profitable these may be (net the initial $13.73 premium). If SPY increases less than $13.73/share, my position loses money. If SPY does not increase at all after 62 days, then my whole investment is lost (albeit only 2.7% of the cost to buy 200 shares outright).

I can only buy as many calls as the free cash in my account will allow (self-imposed guideline: I never want to borrow brokerage funds and owe upwards of 13% interest). Buying calls decreases free cash that may be used for T-bill investing.

Aside from buying calls, another way to participate in the movement of underlying stock is to sell puts. Long (bought) puts generally gain value as the underlying stock falls and sold (short) puts generally gain value as the underlying stock rallies. Selling puts allows me to collect premium rather than paying it; this provides a margin of safety if the underlying stock falls.

As an example, rather than buying the calls previously discussed, suppose I collect the $13.73/share premium by selling the corresponding puts.

The story is now different in several ways:

- First, the premium received for put sales (vs. premium due for call purchase) increases the cash balance in my account that I can use to buy T-bills.

- Second, if SPY increases over 62 days, then I keep the $13.73/share profit (vs. having to overcome any premium paid for profitability).

- Third, $13.73/share is my maximum potential profit (vs. unlimited profit potential net premium paid for long calls).

- Fourth, if SPY decreases up to $13.73/share, then I will have to surrender up to the entire premium received after 62 days. A net loss results if SPY decreases more than $13.73 (vs. long calls that incur maximum loss if SPY goes down at all). Potential loss on the short put is nearly unlimited except for the $13.73/share premium initially received.

I will continue next time.

Categories: Option Trading | Comments (0) | PermalinkInvesting in T-bills (Part 2)

Posted by Mark on February 8, 2024 at 06:56 | Last modified: March 16, 2024 12:02Last time I presented Investopedia information on the basics of T-bills: what they are, how they work, etc. Today I’m going to start discussing why to consider investing in them.

I invest in T-bills to get a better interest rate on cash than I otherwise would. I tend to have free cash in my brokerage account. The brokerage currently pays 0.35% interest on that cash. According to the Bankrate website, the national average yield for savings accounts is 0.57%. T-bills are currently paying over 5.0% interest.

Borrowing brokerage money to invest in T-bills would be a losing proposition. Suppose I open a margin account with $100,000 cash. I can buy stock with $100,000 and T-bills with $50,000. I will make 5% interest on the T-bills, but since that $50,000 is borrowed from the brokerage I will have to pay upwards of 13% interest. This is a guaranteed loss of at least (13% – 5%) = 8%. Bad idea… really bad idea.

For those investing in stocks, T-bills may not add much benefit. A stock investor opens a brokerage account to buy stocks. Most of the cash will therefore be deployed to that end. $95,000 may be used to purchase stock in a $100,000 account. This leaves only $5,000 to buy T-bills. It may still be worthwhile to do so, but T-bill investing does carry a minimal time commitment (to be discussed later).

Because options are leveraged instruments, cash outlays are different. Options allow me to control stock for a fraction of the cost. This means more leftover cash that I can conceivably use to purchase T-bills.

Imagine buying calls in the hypothetical account discussed above. With SPY at $509.83/share, I can buy 200 shares of SPY for $101,966. Alternatively, two 510 calls would cost me $2,746. This allows me to effectively rent 200 shares of SPY for 62 days. My position is then worth the difference of SPY and $510 [multiplied by two (options)]. If SPY is less than $510 then my position expires (i.e. “goes out,” “ends up”) worthless. If SPY is at $524, then my position is ~$2,800 (slight gain). If SPY is at $530, then my position is ~$4,000 [a much larger (percentage) gain].

With calls, I take on the risk of losing the full $2,746, but this is only 2.7% of the cost to buy shares. The leftover cash can be used to purchase T-bills. Interest received would be 0.05 * (100,000 – 2,746) * (62 / 365) ~ $849. With shares, because I borrowed $1,966 to establish the full position, I would actually owe 0.13 * 1,966 * (62 / 365 ) ~ $43 . The difference is $892 in about two months.

Interest aside, at the end of those two months the SPY position could also be down $2,746 were SPY to fall $13.73 (to $496.10/share). While this is an equivalent loss to the option position, I retain ownership of the shares and can subsequently recoup the loss if SPY moves higher. Expiring worthless means the option position can never rebound.

I will continue next time.

Categories: Option Trading | Comments (0) | PermalinkInvesting in T-bills (Part 1)

Posted by Mark on February 5, 2024 at 14:37 | Last modified: March 15, 2024 15:36I find an advantage to investing in Treasury Bills, but I am still trying to wrap my brain around how big a benefit this is, to what extent it may be utilized, and/or how much of it is real or just perceived.

Here are some basics courtesy of Investopedia:

> A Treasury bill [T-bill]… is a short-term U.S. government debt obligation

> backed by the Treasury Department with a maturity of one year or less.

> T-bills are usually sold in denominations of $1,000… These securities are

> widely regarded as low-risk and secure investments.

>

> The U.S. government issues T-bills to fund various public projects, such

> as the construction of schools and highways. When an investor purchases

> a T-bill, the U.S. government effectively writes an IOU to the investor.

> Thus, T-bills are considered a safe and conservative investment since the

> U.S. government backs them.

>

> T-bills are generally held until the maturity date. However, some holders

> may wish to cash out before maturity and realize the short-term interest

> gains by reselling the investment in the secondary market.

>

> T-bills can have maturities of just a few days, but the maturities listed by

> the Treasury are are four, eight, 13, 17, 26, and 52 weeks.

>

> T-bills are issued at a discount from the par value (also known as the face

> value) of the bill, meaning the purchase price is less than the face value of

> the bill. So, for example, a $1,000 bill might cost the investor $950.

>

> When the bill matures, the investor is paid the face value—par value—of

> the bill they bought. If the face value amount exceeds the purchase price,

> the difference is the interest earned for the investor.

>

> T-bills do not pay regular interest payments as with a coupon bond, but a

> T-bill does include interest, reflected in the amount it pays when it matures.

>

> The interest income from T-bills is exempt from state and local income

> taxes. However, the interest income is subject to federal income tax.

>

> New issues of T-bills can be purchased at auctions held by the

> government on the TreasuryDirect site. These are priced through a

> bidding process, with bidders ranging from individual investors to

> hedge funds, banks, and primary dealers. These purchasers may then

> sell the bills to other customers in the secondary market…

>

> You can also buy Treasury bills through a bank or a licensed broker

> [i.e. secondary market]. Once completed, the purchase of the T-bill

> serves as a statement from the government that says you are owed

> the money you invested, according to the terms of the bid.

I will get more into the details of investing with T-bills next time.

Categories: Option Trading | Comments (0) | PermalinkYETI Stock Study (10-26-23)

Posted by Mark on February 2, 2024 at 06:45 | Last modified: March 13, 2024 12:09I recently did a stock study on YETI Holdings (YETI) with a closing price of $41.50. Previous studies are here and here.

M* writes:

> YETI Holdings Inc is a designer, marketer, and distributor of premium

> products for the outdoor and recreation market sold under the YETI

> brand. The company offers products including coolers and equipment,

> drinkware, and other accessories. Its trademark products include YETI,

> Tundra, Hopper, YETI TANK, Rambler, Colster, Rambler Colster, Roadie,

> and Wildly Stronger! Keep Ice Longer!, SideKick, FatWall, PermaFrost,

> T-Rex, ColdLock, NeverFail, AnchorPoint, InterLock, BearFoot, Vortex,

> DoubleHaul, LipGrip, Vortex, DryHide, ColdCell, HydroLock, Over-the-

> Nose, and LOAD-AND-LOCK. The company distributes products through

> wholesale channels and through direct-to-consumer, or DTC, channels.

This medium-size company has grown sales and earnings at annualized rates of 32.5% and 19.3% over the last 9 and 7 years, respectively [’13-’14 EPS excluded due to small fractional values that artificially inflate the growth rate]. The visual inspection is mediocre. Sales are up and straight except for spike in ’15 and decline in ’17. YOY EPS are down in ’16, ’17, ’19, and ’22 [I am excluding the latter 57.1% decline due to operational snafus including recall of defective items and inflation-induced demand destruction per Value Line]. PTPM leads peer and industry averages despite generally trending lower from 12.3% (’13) to 7.3% (’22) with a last-5-year mean of 12.3%.

Over the last four years (too brief a history to compare with peer and industry averages), ROE averages 47.6% and is trending lower. Debt-to-Capital is declining since ’16 and falls below peer/industry averages in ’20 with a last-5-year mean of 50.9% [23.8% in ’22].

Interest Coverage is 22.3 and Quick Ratio is 1.0. Value Line gives a “B+” rating for Financial Strength.

With regard to sales growth:

- CNN Business projects 6.3% YOY and 9.0% per year for ’23 and ’22-’24 (based on 16 analysts).

- YF projects YOY 6.6% and 10.6% for ’23 and ’24, respectively (17 analysts).

- Zacks projects YOY 4.3% and 9.9% for ’23 and ’24, respectively (9).

- Value Line projects 9.4% annualized growth from ’22-’27.

- CFRA projects 6.6% YOY and 8.6% per year for ’23 and ’22-’24, respectively (17).

- M* offers a 2-year annualized ACE of 9.8%.

I am forecasting conservatively toward the bottom of the range at 6.0% per year.

With regard to EPS growth:

- CNN Business projects 7.2% YOY contraction and 7.8% growth per year for ’23 and ’22-’24, respectively (based on 16 analysts), along with 5-year annualized growth of 10.4%.

- MarketWatch projects growth of 7.3% and 10.9% per year for ’22-’24 and ’22-’25, respectively (17 analysts).

- Nasdaq.com projects growth of 22.7% YOY and 16.3% per year for ’24 and ’23-’25 [10/10/1 analyst(s) for ’23/’24/’25].

- Seeking Alpha projects 4-year annualized growth of 10.4%.

- YF projects YOY 3.0% contraction and 19.7% growth for ’23 and ’24 (17) along with 5-year annualized growth of 8.6%.

- Zacks projects YOY 3.0% contraction and 18.3% growth for ’23 and ’24 (11) and 5-year annualized growth of 9.4%.

- Value Line projects annualized growth of 12.2% from ’22-’27.

- CFRA projects 2.3% contraction per year and 4.5% growth per year for ’21-’23 and ’21-’24, respectively (16).

I am forecasting below the long-term-estimate range (mean of five: 10.2%) at 8.0% per year. I will not use ’22 EPS of $1.03/share or 2023 Q2 $0.76/share (annualized) as the initial value since those numbers are affected by [temporary] product recall and production issues. Instead, I will start with ’20 EPS ($1.77) and extrapolate to $1.77 * (1.08 ^ 7) = $3.03/share. I can almost ($3.02/share) get to this as a [website] workaround with a 24.0% growth rate projected from ’22 EPS.

My Forecast High P/E is 31.0. With the stock trading publicly since 2018, high P/E has increased from 31.1 to 80.6 in ’22 for a last-5-year mean of 53.0. The last-5-year-mean average P/E is 36.9. I am forecasting below the range.

My Forecast Low P/E is 16.0. Over the past five years, low P/E ranges from 8.6 (perhaps a downside outlier) in ’20 to 27.0 in ’22 with a last-5-year mean of 20.8. I am forecasting below the latter (18.0 in 2018 being the second-lowest value).

My Low Stock Price Forecast (LSPF) of $28.30 is default based on initial value of $1.77/share. This is 32.7% less than the previous close and 3.7% less than the 52-week low.

These inputs land YETI in the BUY zone with a U/D ratio of 3.5. Total Annualized Return (TAR) is 16.9%.

PAR (using Forecast Average—not High—P/E) of 10.6% is less than I seek for a medium-size company. If a healthy margin of safety (MOS) anchors this study, then I can proceed based on TAR instead.

To assess MOS, I start by comparing my inputs with those of Member Sentiment (MS). Based on only 43 studies (my study and 17 outliers excluded) over the past 90 days, averages (lower of mean/median) for projected sales growth, projected EPS growth, Forecast High P/E, and Forecast Low P/E are 10.0%, 13.0%, 35.0, and 17.7, respectively. I am lower across the board. Value Line’s projected average annual P/E of 20.0 is lower than MS (26.4) and lower than mine (23.5).

MS high / low EPS are $1.66 / $0.76 versus my $3.02 / $1.77 (per share). My EPS range is higher, which is quite rare. I think selection of 2023 Q2 as low EPS is unreasonable since results are still being affected by the recall [per Value Line]. I also don’t understand MS high EPS being less than 2020 EPS (7 years earlier). Value Line’s high EPS is $4.20: higher than mine and ~2.5x MS. What doesn’t surprise me is seeing big differences (and questionable ranges) given such a small MS sample size.

MS LSPF of $15.80 implies a Forecast Low P/E of 20.8: greater than the above-stated 17.7. MS LSPF is 17.5% greater than the default $13.28/share * 17.8 = $13.45, which results in more aggressive zoning. MS LSPF is a whopping 44.2% less than mine. I think MS LSPF is unreasonably low: consistent with skepticism expressed in the last paragraph.

My TAR (over 15.0% preferred) is dramatically higher than the 8.4% from MS. I can’t put much faith in MS given the limited sample size of 43. Comparing my inputs with the analyst estimates and P/E ranges as discussed above, I believe MOS to be moderate or better in the current study.

I track a few different [usually conflicting] valuation metrics. PEG is 2.0 and 1.9 per Zacks and my projected P/E, respectively: slightly overvalued. Relative Value [(current P/E) / 5-year-mean average P/E] of 1.5 (M*) is very high, but I believe it to be skewed by a low ’22 EPS caused by nonrecurring events. Kim Butcher’s “quick and dirty DCF” has the stock 40.4% undervalued: 17.0 * [$4.85 – ($0.00 + $0.70)] = $70.55. I’m skeptical of this as well (big discrepancy).

YETI is a BUY under $44. My main source of reluctance is the rocky visual inspection. As additional MOS, I would look to invest at $44 – 10% (arbitrary) = $39.60/share or less.

Categories: BetterInvesting® | Comments (0) | PermalinkPOOL Stock Study (10-25-23)

Posted by Mark on January 31, 2024 at 06:52 | Last modified: October 25, 2023 11:34I recently did a stock study on Pool Corp. (POOL) with a closing price of $346.78. The original study is here.

CFRA writes:

> Pool Corp. is one of the world’s largest wholesale distributors of

> swimming pool and related backyard products. It is also one of the

> top three distributors of irrigation and related products in the U.S.

> POOL offers a comprehensive selection of services and products

> including: 1) pool maintenance, which includes supplies, repair

> parts and chemicals; 2) pool construction and renovation, which

> includes pool tile, control systems, lighting, pool pumps, filters,

> heaters, cleaners, among others; 3) commercial and residential

> irrigation and landscape equipment and maintenance; 4) outdoor

> living, which includes grills, lighting, and hardscape products.

> Customers primarily include swimming pool remodelers and builders;

> specialty retailers that sell swimming pool supplies; swimming pool

> repair and service businesses; irrigation construction and landscape

> maintenance contractors; and commercial customers who service

> large commercial installations such as hotels, universities, and

> community recreational facilities.

Over the past decade, this medium-size company has grown sales and earnings at annualized rates of 12.3% and 28.0% per year, respectively. Lines are up, mostly straight, and narrowing. PTPM leads peer and industry averages while increasing from 7.6% (’13) to 15.9% (’22) with a last-5-year mean of 12.5%.

Also over the past decade, ROE leads peer and industry averages by increasing from 27.7% (’13) to 61.4% (’22) with a last-5-year mean of 62.1%. Debt-to-Capital is higher than peer and industry averages while ranging from 46.3% in ’13 to 74.9% in ’19 with a last-5-year mean of 60.3%.

Interest Coverage is 11.5 (Value Line) and Current Ratio 2.7 (M*). Value Line gives an “A” rating for Financial Strength.

With regard to sales growth:

- CNN Business projects contraction of 6.5% YOY and 0.8% per year for ’23 and ’22-’24 (based on 12 analysts).

- YF projects YOY 10.1% contraction and 4.0% growth for ’23 and ’24, respectively (11 analysts).

- Zacks projects YOY 10.1% contraction and 4.4% growth for ’23 and ’24, respectively (6).

- Value Line projects 5.3% annualized growth from ’22-’27.

- CFRA projects contraction of 9.8% YOY and 2.6% per year for ’23 and ’22-’24, respectively.

- M* provides a 2-year ACE of 3.3% contraction per year.

My forecast of 2.0%/year discounts the available long-term estimate given the general agreement on shorter-term contraction.

With regard to EPS growth:

- CNN Business projects contraction of 19.2% YOY and 5.1% per year for ’23 and ’22-’24, respectively (based on 12 analysts), along with 5-year annualized contraction of 5.8%.

- MarketWatch projects annualized contraction of 12.6% and 4.9% for ’22-’24 and ’22-’25, respectively (12 analysts).

- Nasdaq.com projects annualized growth of 10.7% and 9.4% for ’23-’25 and ’23-’26 [7/5/1 analyst(s) for ’23/’25/’26].

- Seeking Alpha projects 4-year annualized contraction of 5.8%.

- YF projects YOY 28.7% contraction and 10.4% growth for ’23 and ’24, respectively (7), along with 5-year annualized contraction of 0.8%.

- Zacks projects YOY 27.5% contraction and 8.2% growth for ’23 and ’24, respectively (4), along with 5-year annualized growth of 5.9%.

- Value Line projects annualized growth of 1.4% from ’22-’27.

- CFRA projects contraction of 27.1% YOY and 9.8% per year for ’23 and ’22-’24 along with a 3-year CAGR of 1.0%.

My forecast of -2.0% per year is less than the long-term-estimate mean (-1.0% for five estimates). My initial value will be 2023 Q2 $15.09/share EPS rather than the 2022 EPS of $18.70. For low EPS, I will use a -4.0% growth rate (arbitrary). These result in high and low EPS of $13.64 and $12.30/share, respectively.

My Forecast High P/E is 28.0. Over the past decade, high P/E ranges from 26.5 in ’14 to 43.6 in ’20 with a last-5-year mean of 35.5. The last-5-year average P/E is 27.3. I am forecasting toward the bottom of the range (only ’14 is lower).

My Forecast Low P/E is 18.0. Over the past decade, low P/E goes from 20.9 in ’13 to 22.2 in ’19 before taking a nosedive to 14.9 in ’22. The last-5-year mean is 19.2. I am forecasting toward the bottom of the range [only ’22 and ’20 (17.9) are lower].

My Low Stock Price Forecast (LSPF) is $256.00. Sticking with default gives $221.40, which is 22.0% less than the 52-week low. My Forecast Low P/E is uncertain because I don’t know whether the first or last five years of the past decade will be more representative of the future. Nevertheless, I think the default is too extreme. My LSPF is 20.5% less than the previous close and 9.8% less than the 52-week low. I think that is sufficiently low even from a conservative standpoint.

Over the past decade, Payout Ratio ranges from 18.7% in ’21 to 35.6% in ’13 with a last-5-year mean of 25.6%. I am forecasting below the range at 18%.

These inputs land POOL in the HOLD zone with a U/D ratio of 0.9. Total Annualized Return (TAR) is 4.1%.

PAR (using Forecast Average—not High—P/E) of 0.3% is less than the current yield on T-bills. If a healthy margin of safety (MOS) anchors this study, then I can proceed based on TAR instead (still far below my target).

To assess MOS, I start by comparing my inputs with those of Member Sentiment (MS). Based on only 55 studies (my study and 14 other outliers excluded) over the past 90 days, averages (lower of mean/median) for projected sales growth, projected EPS growth, Forecast High P/E, Forecast Low P/E, and Payout Ratio are 8.8%, 7.9%, 27.3, 18.2, and 27.0%. I am lower on all but Forecast High P/E (28.0). Value Line’s projected average annual P/E of 24.0 is higher than MS (22.8) and mine (23.0).

MS high / low EPS are $23.98 / $15.09. My EPS range (see above) is lower. Value Line’s high EPS is $20.00.

MS LSPF of $260.30 implies a Forecast Low P/E of 17.2: less than the above-stated 18.2. MS LSPF is 5.2% less than the default $15.09/share * 18.2 = $274.64, which results in more conservative zoning. MS LSPF is still 1.7% greater than mine.

My TAR (over 15.0% preferred) is much less than the 15.6% from MS. MOS seems robust in the current study.

I track a few different [usually conflicting] valuation metrics. PEG is 4.1 per Zacks: significantly overvalued. Relative Value [(current P/E) / 5-year-mean average P/E] per M* is cheap at 0.6. Kim Butcher’s “quick and dirty DCF” suggests the stock to be 15.3% undervalued: 21.0 * [$5.00 – ($6.00 + $0.90)] = $380.10/share.

POOL is a BUY under $287. With a forecast high price near $382, TAR should meet my 15% criterion around $191/share.

My investment outlook will improve dramatically if/when [most/all] analysts start seeing growth back on the horizon. Until then, it’s not a high-quality BI stock anyway.

Categories: BetterInvesting® | Comments (0) | PermalinkNFLX Stock Study (10-24-23)

Posted by Mark on January 29, 2024 at 06:45 | Last modified: October 24, 2023 10:14I recently did a stock study on Netflix Inc. (NFLX) with a closing price of $406.84. Previous studies are here, here, and here.

M* writes:

> Netflix’s primary business is a streaming video on demand

> service now available in almost every country worldwide

> except China. The firm primarily generates revenue from

> subscriptions to its eponymous service. Netflix delivers

> original and third-party digital video content to PCs,

> internet-connected TVs, and consumer electronic devices,

> including tablets, video game consoles, Apple TV, Roku,

> and Chromecast. Netflix is the largest SVOD platform in

> the world with over 220 million subscribers globally.

Over the past decade, this large-size company has grown sales and earnings at annualized rates of 26.6% and 58.4%, respectively. Lines are mostly up, narrowing, and parallel except for EPS declines in ’15 and ’22. PTPM lags peer and industry averages despite trending higher from 3.9% (’13) to 16.6% (’22) with a last-5-year mean of 13.4%.

Also over the past decade, ROE lags peer and industry averages despite trending up from 9.2% (’13) to 21.6% (’22) with a last-5-year mean of 26.0%. Debt-to-Capital is roughly even with peer and industry averages while increasing from 27.3% in ’13 to 66.4% in ’18 then reversing lower to 40.9% in ’22 for a last-5-year mean of 56.5%.

Interest Coverage and Quick Ratio are 7.5 and 1.1, respectively. M* gives the company a “Standard” rating for Capital Allocation while Value Line gives an A rating for Financial Strength.

With regard to sales growth:

- CNN Business projects 7.3% YOY and 10.2% per year for ’23 and ’22-’24, respectively (based on 39 analysts).

- YF projects YOY 0.3% and 13.9% for ’23 and ’24, respectively (37 analysts).

- Zacks projects YOY 6.2% and 13.6% for ’23 and ’24, respectively (14).

- Value Line projects 9.9% growth per year from ’22-’27.

- CFRA projects 6.4% YOY and 9.9% per year for ’23 and ’22-’24, respectively.

- M* provides a 2-year ACE of 10.0%/year while projecting 5-year annualized growth of 8.0% in its analyst note.

I am forecasting toward the low end of the range at 6.0% per year.

With regard to EPS growth:

- CNN Business projects 16.0% YOY and 23.0% per year for ’23 and ’22-’24, respectively (based on 39 analysts), along with 5-year annualized growth of 28.9%.

- MarketWatch projects annualized ACE of 24.2% and 23.8% for ’22-’24 and ’22-’25, respectively (48 analysts).

- Nasdaq.com projects 25.1% and 19.8% per year for ’23-’25 and ’23-’26 (15, 12, and 4 analysts for ’23, ’25, and ’26).

- Seeking Alpha projects 4-year annualized growth of 23.1%.

- YF projects YOY 14.6% and 29.6% for ’23 and ’24, respectively (38), along with 5-year annualized growth of 23.0%.

- Zacks projects YOY 21.1% and 31.6% for ’23 and ’24, respectively (14), along with 5-year annualized growth of 21.3%.

- Value Line projects annualized growth of 13.6% from ’22-’27.

- CFRA projects 22.6% YOY and 26.0% per year for ’23 and ’22-’24, along with a 3-year CAGR of 20.0%.

- M* gives a long-term annualized growth estimate of 15.8%.

I am forecasting just under the long-term-estimate range (mean of six: 21.0%) at 13.0% per year. I will use 2023 Q2 EPS of $9.39/share (annualized) as the initial value rather than ’22 EPS of $9.95.

My Forecast High P/E is 35.0. Over the past decade, high P/E has decreased from 211 (’13) to 61.3 (’22) with a last-5-year mean of 93.9. The last-5-year-mean average P/E is 71.0. At some point, I expect P/E to fall back to earth. For now, I am forecasting at the upper end of my comfort zone.

My Forecast Low P/E is 30.0. Over the past decade, low P/E has decreased from 49.1 (’13) to 16.4 (’22) with a last-5-year mean of 48.1. Again, at some point I expect P/E to fall back to earth and we may already be starting to see this with a current P/E of 43.3. I am forecasting toward the bottom of the range (only ’22 is lower).

My Low Stock Price Forecast (LSPF) is $281.70: default based on $9.39/share initial value. This is 30.8% less than the previous close but 11.7% greater than the 52-week low.

These inputs land NFLX in the HOLD zone with a U/D ratio of 1.6. Total Annualized Return (TAR) is 8.3%.

PAR (using Forecast Average—not High—P/E) of 6.7% is less than I seek for a large-size company. If a healthy margin of safety (MOS) anchors this study, then I can proceed based on TAR instead.

To assess MOS, I compare my inputs with those of Member Sentiment (MS). Based on 182 studies (my study and 40 outliers excluded) over the past 90 days, averages (lower of mean/median) for projected sales growth, projected EPS growth, Forecast High P/E, and Forecast Low P/E are 10.0%, 12.9%, 48.5, and 30.0. I am lower on the first and third but slightly higher on the second (13.0%). Value Line’s projected average annual P/E of 38.0 is lower than MS (39.3) and higher than mine (32.5).

MS high / low EPS are $17.54 / $9.27 versus my $17.30 / $9.39 (per share). My high EPS is lower due to a lower growth rate. Value Line’s high EPS is $18.85. I am lowest of the three.

MS LSPF of $225 implies a Forecast Low P/E of 24.3: less than the above-stated 30.0. MS LSPF is 19.1% less than the default $9.27/share * 30.0 = $278.10, which results in more conservative zoning. MS LSPF is also 20.1% less than mine.

My TAR (over 15.0% preferred) is much less than the 16.3% from MS. MOS seems robust in the current study.

I track a few different [usually conflicting] valuation metrics. PEG is 1.3 and 2.9 per Zacks and my projected P/E, respectively: the latter significantly overvalued. Relative Value [(current P/E) / 5-year-mean average P/E] per M* is cheap at 0.6. Kim Butcher’s “quick and dirty DCF” prices the stock at 12.0 * [$18.85 – ($0.00 + $1.25)] = $211.20: overvalued by 48.1%.

NFLX is a BUY under $362. With a forecast high price of $605.50, TAR should meet my 15% criterion around $303/share.

Categories: BetterInvesting® | Comments (0) | PermalinkMBUU Stock Study (10-23-23)

Posted by Mark on January 25, 2024 at 06:46 | Last modified: October 23, 2023 10:25I recently did a stock study on Malibu Boats Inc. (MBUU, $50.00). Previous studies are here and here.

M* writes:

> Malibu Boats is a leading designer and manufacturer of power

> boats in the United States. It is the market leader in

> performance sport boats, sold under its Malibu and Axis brands.

> It acquired Cobalt Boats, a leading producer of sterndrive

> boats in the U.S. in the 24-foot to 29-foot segment, and

> Pursuit Boats, which makes high-end offshore and outboard

> motorboats in 2018. In 2021, it purchased Maverick Boat Group,

> a leading seller of flat fishing boats, with exposure to bay,

> dual-console, and center-console boats. Malibu has also

> expanded into boat trailers and accessories, and in 2020

> began producing its own engines (Monsoon) for its performance

> sport boats. Malibu’s target market includes a wide range of

> water enthusiasts who embrace the active outdoor lifestyle.

Over the past decade, this medium-size company has grown sales and earnings at annualized rates of 26.6% and 30.5% [86.0% if the 2014 loss is included], respectively. Lines are mostly up, straight, and parallel except for a sales decline in ’20 (FY ends Jun 30) and EPS declines in ’18, ’20, and ’23. PTPM is higher than peer and industry averages, ranging from 10.2% in ’23 (excluding the loss from ’14) to 18.0% in ’18 with a last-5-year mean of 13.9%.

Over the past five years, ROE is slightly better than peer and industry averages despite falling from 35.6% in ’19 to 16.7% in ’23 with a mean of 28.6%. Debt-to-Capital is lower than peer and industry averages by falling from 35.7% in ’19 to 0.4% in ’23 with a last-5-year mean of 21.7%.

Interest Coverage is 48.8 and Quick Ratio is 0.63. M* rates the company “Standard” for Capital Allocation while Value Line assigns a B+ rating (down from B++ last quarter) for Financial Strength. The company currently has zero long-term debt.

With regard to sales growth:

- CNN Business projects contraction of 14.3% YOY and 3.6% per year for ’24 and ’23-’25 (based on 7 analysts).

- YF projects YOY 16.7% contraction and 6.4% growth for ’24 and ’25, respectively (8 analysts).

- Zacks projects YOY 16.8% contraction and 4.6% growth for ’24 and ’25, respectively (4).

- Value Line projects 0.2% annualized growth from ’23-’27.

- CFRA projects contraction of 16.6% YOY and 5.9% per year for ’24 and ’23-’25, respectively (8).

- M* gives 2-year annualized ACE of 3.9% contraction and projects growth of 5.0%/year x5 years (analyst note).

I am forecasting less than both long-term estimates at 0%.

With regard to EPS growth:

- CNN Business projects contraction of 19.0% YOY and 8.7% per year for ’24 and ’23-’25, respectively (based on 7 analysts), along with a 5-year annualized growth of 10.1%.

- MarketWatch projects contraction of 29.9% YOY and 11.1% per year for ’24 and ’23-’25, respectively (8 analysts).

- Nasdaq.com projects 11.3% YOY growth for ’25 (4).

- YF projects YOY 34.4% contraction and 14.3% growth for ’24 and ’25, respectively (8), along with 5-year annualized growth of 15.0%.

- Zacks projects YOY 33.3% contraction and 10.8% growth for ’24 and ’25, respectively (4).

- Value Line projects 2.5% annualized contraction from ’23-’27.

- CFRA projects growth of 19.2% YOY and 16.7% per year for ’24 and ’23-’25, respectively (7).

- M* projects long-term annualized growth of 5.8%.

I am forecasting toward the bottom of the long-term-estimate range (mean of four: 7.1%). I will use ’23 EPS of $5.06/share as the initial value.

My Forecast High P/E is 12.0. Since 2015, high P/E falls from 26.0 (34.2 in ’18 excluded) to 14.0 (’23) with a last-5-year mean of 16.3. The last-5-year-mean average P/E is 12.2. I am forecasting below the latter [only ’22 is lower (11.5)].

My Forecast Low P/E is 7.0. Since 2015, low P/E generally trends down from 17.4 to 9.2 (’23) with a last-5-year mean of 8.1. I am forecasting toward the bottom of the range [only 6.1 (’20) and 6.4 (’22) are lower].

My Low Stock Price Forecast (LSPF) is $35.40: default based on $5.06/share initial value. This is 29.2% less than the previous close and 24.0% less than the 52-week low.

These inputs land MBUU in the HOLD zone with a U/D ratio of 1.6. Total Annualized Return (TAR) is 8.1%.

PAR (using Forecast Average—not High—P/E) is 3.2%, which is less than the current yield on T-bills. If a healthy margin of safety (MOS) anchors this study, then I can proceed based on TAR instead.

To assess MOS, I compare my inputs with those of Member Sentiment (MS). Based on 196 studies (my study and 29 outliers excluded) over the past 90 days, averages (lower of mean/median) for projected sales growth, projected EPS growth, Forecast High P/E, and Forecast Low P/E are 9.0%, 8.9%, 14.0, and 7.6, respectively. I am lower across the board. Value Line’s projected average annual P/E of 10.0 is lower than MS (10.8) and higher than mine (9.5).

MS high / low EPS are $8.82 / $5.06 versus my $6.16 / $5.06 (per share). My high EPS is lower due to a lower growth rate. Value Line’s high EPS is $8.30. I am lowest of the three.

MS LSPF of $38.20 implies a Forecast Low P/E of 7.5, which is consistent with above. MS LSPF is 7.9% greater than mine thereby implying more aggressive zoning.

My TAR (over 15.0% preferred) is much less than the 20.2% from MS. MOS seems robust in the current study.

I track a few different [usually conflicting] valuation metrics. PEG per my projected P/E is overvalued at 2.4. Relative Value [(current P/E) / 5-year-mean average P/E] per M* is slightly undervalued at 0.8. Kim Butcher’s “quick and dirty DCF” prices the stock at 8.0 * [$10.05 – ($0.00 + $2.60)] = $59.60, which suggests the stock to be 15.9% undervalued.

MBUU is a BUY under $45. With a forecast high price near $74, TAR should meet my 15% criterion around $37/share.

Categories: BetterInvesting® | Comments (0) | PermalinkTGT Stock Study (10-20-23)

Posted by Mark on January 23, 2024 at 07:05 | Last modified: October 20, 2023 12:17I recently did a stock study on Target Corp. (TGT) with a closing price of $108.36. Previous studies are here, here, and here.

CFRA writes:

> Incorporated in 1902 and headquartered in Minneapolis, Target

> Corporation is one of the largest retailers in the U.S. As of

> January 29, 2022, the company operated 1,926 Target locations

> in the U.S. with 243.3 million square feet of floor space, up

> from 1,897 stores with 241.6 million square feet of floor

> space twelve months earlier. Target currently has stores in

> all 50 states and the District of Columbia. Its stores

> generally cater to middle- and upper-income consumers,

> carrying a broad assortment of fashion apparel, electronics,

> home furnishings, household products, and other general

> merchandise. Target.com offers a more extensive selection of

> merchandise than the company’s physical stores, including

> exclusive online products.

Over the past decade, this mega-sized company (revenue > $50B) has grown sales and earnings at annualized rates of 4.9% and 11.9%, respectively (FY ends Jan 31). Lines are mostly up except for dips in sales (’17) and EPS (’17 and ’23). PTPM leads peer and industry averages throughout the decade despite a disappointing ’23 contributing to a last-5-year mean of 5.5%.

Also over the past decade, ROE leads peer and industry averages by increasing from 12.0% (’14) to 25.0% (’23) with a last 5-year mean of 31.9%. Debt-to-Capital is higher than peer and industry averages, increasing from 45.9% (’14) to 62.9% (’23) with a last-5-year mean of 55.7%.

Quick Ratio is chronically low (0.08 in the last quarter), but Interest Coverage is 8.8. Value Line gives a B++ rating for Financial Strength while M* assigns an “Exemplary” rating for Capital Allocation.

With regard to 2023 EPS decline, Value Line wrote:

> Followers of this story will recall that the bottom line last year

> was torpedoed when management announced a serious inventory

> bloat would be worked down by across-the-board discounting.

> Shortly thereafter, a clearance run event was held to get

> shoppers to spend at the tail end of the holiday season, thus

> again clearing inventory space for items geared toward warmer

> weather. The end result was a sharp drop in profitability and

> a full-year earnings figure of just $5.98 a share.

With regard to sales growth:

- CNN Business projects 0.9% YOY and 1.3% per year for ’24 and ’23-’25 (based on 29 analysts).

- YF projects YOY 1.8% contraction and 0.8% growth for ’24 and ’25, respectively (29 analysts).

- Zacks projects YOY 1.8% contraction and 0.6% growth for ’24 and ’25, respectively (13).

- Value Line projects 3.2% annualized growth from ’23-’28.

- CFRA projects contraction of 1.8% YOY and 0.4% per year for ’24 and ’23-’25, respectively.

- M* gives a 2-year ACE of 0.8% contraction per year.

I am forecasting less than the long-term estimate at 1.0% per year.

With regard to EPS growth:

- CNN Business projects 36.0% YOY and 30.0% per year for ’24 and ’23-’25, respectively (based on 29 analysts), along with 5-year annualized growth of 15.0%.

- MarketWatch projects 27.3% and 21.8% per year for ’23-’25 and ’23-’26, respectively (36 analysts).

- Nasdaq.com projects 18.3% YOY and 14.3% per year for ’25 and ’24-’26 (17, 17, and 7 analysts for ’24, ’25, and ’26).

- Seeking Alpha projects 4-year annualized growth of 13.4%.

- YF projects YOY 25.7% and 18.5% for ’24 and ’25 (30) along with 5-year annualized growth of 18.3%.

- Zacks projects YOY 25.9% and 18.3% for ’24 and ’25 (17) along with 5-year annualized growth of 12.7%.

- Value Line projects 23.2% growth per year from ’23-’28.

- CFRA projects 23.3% YOY and 17.8% per year for ’24 and ’23-’25 along with a 3-year CAGR of -15.0% [NOTE: the 3 years must begin (a long-time curiosity of mine) in ’22 as discounting $13.56/share by 15%/year results in $8.33 for ’25, which is very close to the stated $8.35/share].

- M* projects long-term annualized growth of 15.7%.

The long-term estimates are dramatically higher than three months ago. The mean (of six) has increased from 10.3% to 16.4%. This is primarily due to two negative estimates (Seeking Alpha at -0.6% and YF at -7.5%) that are now significantly positive. It’s almost mind-boggling to imagine the arithmetic average of ~30 analysts changing so much over one quarter. I sometimes wonder if I’m looking at data importation errors on the website. One such error, which could never actually be confirmed, can dramatically affect my forecast.

I am forecasting below the long-term-estimate range at 12.0% per year. I will use ’23 EPS of $5.98 as the initial value. Three months ago, I went with the trendline since $5.98/share—down 57.6% YOY—seemed unreasonably low. Owing largely to the negative long-term estimates just discussed, however, three months ago my forecast EPS growth rate was only 4.0%.

My Forecast High P/E is 15.0. Over the past decade, high P/E ranges from 14.8 (’18) to 42.6 (upside outlier in ’23) with a last-5-year mean (excluding the outlier) of 19.8. The last-5-year-mean average P/E is 15.4. I am forecasting near the bottom of the range (only ’18 is lower).

My Forecast Low P/E is 10.5. Over the past decade, low P/E ranges from 9.1 (’18) to 22.9 (’23). Low P/E has been 14.2 or less since ’15, which makes the 22.9 seem like an outlier. Excluding that, the last-5-year mean is 11.0. I am forecasting near the bottom of the range [only ’18 and ’21 (10.4) are lower].

My Low Stock Price Forecast (LSPF) is $80.00. This is a rare instance where the default value of $62.80 is unreasonably low. That would be 42.0% less than the previous close and a whopping 39.0% less than the 52-week low. The stock has already fallen 59.7% from its all-time high (2021) and with EPS cratering in ’23, growth is expected moving forward. Sticking with the default in this case feels like trying to fit a square peg in a round hole. Instead, I am going with a price 26.2% less than the previous close and 22.3% less than the 52-week low. In my opinion, that is still conservative.

Over the past decade, Payout Ratio ranges from 22.4% (’22) to 66.2% (’23). The last-5-year mean is 41.3%. I am forecasting below the range at 22.0%.

These inputs land TGT in the HOLD zone with a U/D ratio of 1.8. Total Annualized Return (TAR) is 9.3%.

PAR (using Forecast Average—not High—P/E) of 6.1% is less than I seek for a mega-size company. If a healthy margin of safety (MOS) anchors the study, then I can proceed based on TAR instead.

To assess MOS, I compare my inputs with those of Member Sentiment (MS). Based on 120 studies (my study and 62 outliers excluded) over the past 90 days, averages (lower of mean/median) for projected sales growth, projected EPS growth, Forecast High P/E, Forecast Low P/E, and Payout Ratio are 3.7%, 10.0%, 19.0, 11.5, and 41.3%, respectively. I am lower on all but EPS growth (12.0%). Value Line’s projected average annual P/E of 15.0 is just lower than MS (15.8) and higher than mine (12.8).

MS high / low EPS are $11.32 / $6.89 versus my $10.54 / $5.98 (per share). My high EPS is lower due to a lower growth rate. Value Line’s high EPS is $17.00. I am lowest of the three.

MS LSPF of $92.20 implies a Forecast Low P/E of 13.4: more than the above-stated 11.5. MS LSPF is 16.4% greater than the default $11.32/share * 11.5 = $79.24, which results in more aggressive zoning. Like mine, other studies may also have overridden default to select a higher LSPF. MS LSPF is 15.3% greater than mine.

My TAR (over 15.0% preferred) is much less than MS 15.3%. MOS seems robust in the current study.

I track a few different valuation metrics. PEG is 1.1 per Zacks and my projected P/E: fairly valued. Relative Value per M* [(current P/E) / 5-year-mean average P/E] is fair at 1.0. Although these metrics often conflict, they are quite consistent here.

TGT is a BUY under $99. With a forecast high price around $158, TAR should meet my 15% criterion around $79/share.

Categories: BetterInvesting® | Comments (0) | PermalinkDG Stock Study (10-19-23)

Posted by Mark on January 19, 2024 at 06:19 | Last modified: October 19, 2023 11:01I recently did a stock study on Dollar General Corp. (DG) with a closing price of $116.02. Previous studies are here and here.

M* writes:

> A leading American discount retailer, Dollar General operates

> over 19,000 stores in 47 states, selling branded and private-

> label products across a wide variety of categories. In fiscal

> 2022, 80% of net sales came from consumables (including paper

> and cleaning products, packaged and perishable food, tobacco,

> and health and beauty items), 11% from seasonal merchandise

> (such as toys, greeting cards, decorations, and gardening

> supplies), 6% from home products (for example, kitchen

> supplies, small appliances, and cookware), and 3% from

> apparel. Stores average roughly 7,500 square feet, and about

> 75% of Dollar General locations are in towns of 20,000 or

> fewer people. The firm emphasizes value, with most of its

> items sold at everyday low prices of $5 or less.

Over the past decade, this large-size company has grown sales and EPS at annualized rates of 9.1% and 16.1%, respectively. Lines are up, straight, and parallel except for an EPS dip in ’22. PTPM leads peer and industry averages while decreasing from 9.3% (’14) to 8.2% (’23) with a last-5-year mean of 8.6% (FY ends Jan 31).

Also over the past decade, ROE leads peer and industry averages while trending higher from 19.1% (’14) to 39.2% (’23) with a last-5-year mean of 32.7%. Debt-to-Capital is less than peer and industry averages until ’20 when it spikes higher and continues to increase. The last-5-year mean is somewhat uncomfortable at 61.4%.

Despite a Quick Ratio of only 0.08, Current Ratio is 1.39 and Interest Coverage is 10.5. Value Line gives an A rating for Financial Strength. M* gives a “Standard” rating for Capital Allocation and writes:

> Dollar General has featured a sound balance sheet

> historically, and we see little reason for solvency concerns

> moving forward as we look at the firm’s midterm prospects.

With regard to sales growth:

- CNN Business projects 4.0% YOY and 5.4% per year for ’24 and ’23-’25, respectively (based on 27 analysts).

- YF projects YOY 1.9% and 5.3% for ’24 and ’25, respectively (25 analysts).

- Zacks projects YOY 2.3% and 5.3% for ’24 and ’25, respectively (10 [sic?]).

- Value Line projects 4.0% annualized growth from ’23-’28.

- CFRA projects 2.3% YOY and 4.5% per year for ’24 and ’23-’25, respectively.

- M* offers a 2-year ACE of 3.4%/year.

I am forecasting near the bottom of the range at 2.0% per year.

With regard to EPS growth:

- CNN Business reports ACE of 5.7% YOY contraction and 1.3% growth per year for ’24 and ’23-’25, respectively (based on 27 analysts), along with 5-year annualized contraction of 6.1%.

- MarketWatch projects annualized contraction of 14.8% and 7.1% for ’23-’25 and ’23-’26, respectively (33 analysts).

- Nasdaq.com projects annualized growth of 9.5% and 11.7% for ’24-’26 and ’24-’27, respectively (17, 15, and 5 analysts for ’24, ’26, and ’27).

- Seeking Alpha projects 4-year annualized contraction of 4.9%.

- YF projects YOY 29.9% contraction and 3.6% growth for ’24 and ’25, respectively (27), along with 5-year annualized contraction of 6.5%.

- Zacks projects YOY 28.5% contraction and 4.1% growth for ’24 and ’25, respectively (23), along with 5-year annualized growth of 7.2%.

- Value Line projects 2.0% annualized growth from ’23-’28.

- CFRA projects contraction of 30.5% YOY and 11.1% per year for ’24 and ’23-’25, respectively, along with a 3-year projected CAGR of -6.0%.

- M* projects long-term annualized growth of 6.5%.

I am forecasting just below the mean long-term estimate (-0.3%) at -1.0% per year. This is not conservative unless one is convinced the company will grow long-term earnings. Analyst long-term estimates are split with three each siding for growth and contraction. I will use 2024 Q2 EPS of $9.76 (annualized) rather than ’23 EPS of $10.68/share to get a high EPS of 9.76 * (0.99 ^ 5) = $9.28/share. As low EPS, $9.76 * (0.97 ^ 5) = $8.38/share uses a -3.0% [arbitrary] growth rate.

My Forecast High P/E is 19.0. Over the past decade, high P/E increases from 19.9 (’14) to 24.6 (’23) with a last-5-year mean of 22.9. The last-5-year-mean average P/E is 19.1. I am forecasting near the bottom of the range (only 18.8 in ’17 is lower).

My Forecast Low P/E is 11.0. Over the past decade, low P/E ranges from 11.7 in ’18 to 17.2 in ’23 with a last-5-year mean of 15.3. I am forecasting below the entire range.

My Low Stock Price Forecast (LSPF) of $92.20 is default based on low EPS of $8.38/share. This is 20.5% less than the previous close and 8.8% less than the 52-week low.

Since a dividend was first issued in ’16, Payout Ratio ranges from 13.6% in ’21 to 22.6% in ’17. I am forecasting below the range at 13.0%.

These inputs land DG in the HOLD zone with a U/D ratio of 2.5. Total Annualized Return (TAR) is 9.4%.

PAR (using Forecast Average—not High—P/E) of 4.6% is less than the current yield on T-bills. If a healthy margin of safety (MOS) anchors this study, then I can proceed based on TAR instead.

To assess MOS, I compare my inputs with those of Member Sentiment (MS). Based on 210 studies (my study and 102 other outliers excluded) over the past 90 days, averages (lower of mean/median) for projected sales growth, projected EPS growth, Forecast High P/E, Forecast Low P/E, and Payout Ratio are 6.0%, 8.2%, 21.3, 14.4, and 17.9%, respectively. I am lower across the board. Value Line’s projected average annual P/E of 19.0 is higher than MS (17.9) and higher than mine (16.0).

MS high / low EPS are $15.33 / $9.96 versus my $9.28 / $8.38 (per share). Despite mentioning above that my forecast growth rate is not conservative, my EPS range is completely below MS thereby suggesting it may be more conservative than I think. Value Line’s high EPS is $11.80. I am lowest of the three.

MS LSPF of $130.30 (invalid on today’s date) implies a Forecast Low P/E of 13.1: less than the above-stated 14.4. MS LSPF is 9.2% less than the default $9.96/share * 14.4 = $143.42 (also invalid on today’s date), which results in more conservative zoning. MS LSPF is still 41.3% greater than mine.

My TAR (over 15.0% preferred) is much less than MS 21.7%. MOS seems robust in the current study.

I track a few different [usually conflicting] valuation metrics. PEG (Zacks) is overvalued at 2.1. Relative Value [(current P/E) / 5-year-mean average P/E] per M* is cheap around 0.6. Kim Butcher’s “quick and dirty DCF” suggests the stock to be 51.0% overvalued with a fair value of: 14.5 * [$15.00 – ($2.68 + $8.40)] = $56.84 [from 2023 10-K, $1.9B projected ’24 Capex / 226.3M diluted shares outstanding = $8.40—and even that is likely less than the 5-year projection].

DG is a BUY under $113. With a forecast high price near $176, TAR should meet my 15% criterion around $88/share.

Categories: BetterInvesting® | Comments (0) | Permalink