GNRC Stock Study (2-6-23)

Posted by Mark on October 27, 2022 at 06:40 | Last modified: March 2, 2023 14:33I recently* did a stock study on Generac Holdings Inc. (GNRC) with a closing price of $122.44.

M* writes:

> Generac Power Systems designs and manufactures power generation

> equipment serving residential, commercial, and industrial markets.

> It offers standby generators, portable generators, lighting,

> outdoor power equipment, and a suite of clean energy products.

This medium-sized company has grown sales and earnings at annualized rates of 11.2% and 18.6%, respectively, over the last 10 years. Lines are mostly up and parallel except for sales/EPS declines in ’14 and ’15 along with EPS decline in recent quarters. PTPM has been cyclical—ranging from 9.3% (’15) to 18.8% (’13) with a last-5-year average of 15.7%. This is higher than peer (stated as SPXC, IR, and GTES) and industry averages.

Excluding an upside outlier of 66.9% in ’13, ROE has ranged from 15.1% (’15) to 38.3% (’14) with a last-5-year average of 30%. This leads peer and industry averages. Debt-to-Capital has trended lower since 2012 from 65.8% to 37.4% with a last-5-year average of 49.1%. This is mostly higher than peer and industry averages. Interest Coverage is 14 and Current Ratio is 2.1 (sans inventory, the Quick Ratio is 0.70).

I assume long-term annualized sales growth of 7% based on the following:

- CNN Business projects growth of 24.3% YOY and 6.5% per year for ’22 and ’21-’23, respectively (based on 20 analysts).

- YF projects 22.5% YOY growth and 8.6% YOY contraction for ’22 and ’23, respectively (22 analysts).

- Zacks projects YOY growth of 22.7% and YOY contraction of 7.1% for ’22 and ’23, respectively (7).

- Value Line projects annualized growth of 18.4% from ’21-’26.

- CFRA projects growth of 24% YOY and 15.2% per year for ’23 and ’22-’24, respectively.

- M* provides a 2-year growth estimate of 7%.

I assume long-term annualized EPS growth of 5% based on the following:

- CNN Business projects contraction of 12.5% YOY and 13.4% per year for ’22 and ’21-’23, respectively (based on 20 analysts) along with 5-year annualized growth of 10%.

- MarketWatch projects contraction of 13.2% and 4% per year for ’21-’23 and ’21-’24, respectively (25 analysts).

- Nasdaq.com projects annualized growth of 2.1% and 5.4% for ’22-’24 and ’22-’25, respectively (7, 10, and 3 analysts).

- Seeking Alpha projects 5-year annualized growth at 10%.

- YF projects YOY contraction of 10.9% and 15% for ’22 and ’23, respectively, along with 5-year annualized contraction of 1.4% (22).

- Zacks projects YOY contraction of 11.7% and 14.2% for ’22 and ’23, respectively, along with 5-year annualized growth of 10% (11).

- Value Line projects annualized growth of 20.4% from ’21-’26.

- CFRA projects 2.9% YOY contraction and 2.7% growth per year for ’23 and ’22-’24, respectively, along with a 3-year annualized growth of 12%.

- M* gives a long-term annualized growth ACE of 6.7%.

My projected growth rate is somewhat of a compromise. Seeing that ’22 is not complete, my guess is that analyst long-term estimates are based on the last annualized number. As this effectively raises the High Stock Price Forecast, I will do so with a lower growth forecast: 5% rather than 6%.

My Forecast High P/E is 22. Over the last 10 years, high P/E has ranged from 17.1 (’18) to 63.2 (upside outlier in ’21) with a last-5-year average (excluding the outlier) of 26.7.

My Forecast Low P/E is 12. Over the last 10 years, low P/E has ranged from 12 (’19) to 26.8 (upside outlier in ’21) with a last-5-year average (excluding the outlier) of 12.8.

My Low Stock Price Forecast of $79.80 is the default value. This is about 35% below the last closing price and 7.5% lower than the 52-week low price.

All this results in an U/D ratio of 2.6, which makes GNRC a HOLD. The Total Annualized Return (TAR) computes to 13.7%.

PAR is 8%, which is a bit lower than I’d like to see for a medium-sized company.

I use member sentiment (MS) to assess margin of safety (MOS) in deciding how likely it is that TAR rather than PAR can be realized. Out of 378 studies over the past 90 days (excluding my own along and 50 others with invalid low prices), projected sales growth, projected EPS growth, Forecast High P/E, and Forecast Low P/E average 11%, 12%, 24.8, and 14.3, respectively. I am lower on all inputs. Value Line’s estimate, perhaps the most optimistic of all, seems like an upside outlier. They project a future average annual P/E of 27.5, which far outpaces my 17 and is also higher than MS 19.5.

MOS appears to be alive and well in this study.

MS Low Stock Price Forecast is $84.33: 5.7% above my own. This is not unreasonable and would put me just on the cusp of the BUY zone. I am sticking with my Forecast Low P/E, however, which results in a HOLD on these shares at $118 or higher.

*—Publishing in arrears as I’ve been doing one daily stock study while posting only two blogs per week.

Backtester Development (Part 1)

Posted by Mark on October 24, 2022 at 06:40 | Last modified: June 22, 2022 08:35This mini-series will be a chronicle of backtester development activities. Because so many things are a Python learning experience for me, I think it’s worth documenting them for later review.

I want to start by revisiting the problem I was having with data type conversion. I noted ignorance as to why the problem occurs. My partner filled me in:

> I think this is an excel issue. Do a right click on the file and use the “open

> with” option. Use Notepad. You will see that everything is displayed as float…

> When you open either file with excel, excel creates what looks like an integer.

In other words, this is not actually a problem. Excel makes things look nice, which in this case created an unintentional headache. Having to reformat data from a commercialized vendor source to serve my own purpose should not be surprising.

In the post linked above, I also presented some additional lines to record program duration in a log file. I couldn’t understand why the output data separated by commas was not printing to separate cells in the Excel .csv.

The explanation is the difference between the following two lines:

The commas in L305 are visible only to the Python program. In order to be visible to the application displaying the .csv file, I need to include quotation marks around the commas as if I were printing them (L307).

I enclosed the entire program in a while loop with a new variable timing_count in order to have the program run three times and log multiple elapsed times.

I then assigned current_date in find_long and reset the variable as part of the else block in L77. These were suggestions from Part 11. The program output appears unchanged. Run duration appears consistent and relatively unchanged (as best as I can tell when comparing two sets of three elapsed times each).

The next step is to add the check_second flag (discussed in Part 5), which ended up as a total mess because subsequent debugging took over two hours to seek out a “stupid mistake” (grade-school math terminology) I made in the process.

To refresh your memory especially with regard to the DTE criterion, see second paragraph of Part 6.

My approach to the check_second flag is as follows:

- The previous find_long block is split in two: check_second == False and ELSE (implies check_second == True).

- False includes a nested if statement that checks DTE criterion (ELSE CONTINUE), 10-multiple criterion, then strike price and 10-multiple (redundant) criteria followed by complete variable assignment including flipping check_second to True.

- True (ELSE block) includes a nested if statement that checks for a change in DTE (ELSE CONTINUE), DTE criterion, 10-multiple criterion, then strike price and 10-multiple (redundant) criteria followed by partial variable assignment (SPX price and strike price already assigned), resetting of check_second, assigning find_short to control_flag, and CONTINUE.

- The DTE criterion of True has ELSE block that includes: check_second reset, control_flag = find_short, and CONTINUE.

I will resume next time.

Categories: Python | Comments (0) | PermalinkPKG Stock Study (2-3-23)

Posted by Mark on October 21, 2022 at 07:04 | Last modified: March 1, 2023 14:48I recently* did a stock study on Packaging Corp. of America (PKG) with a closing price of $145.09.

M* writes, “Packaging Corp of America is the third-largest containerboard and corrugated packaging manufacturer in the United States.”

This medium-sized company has grown sales and earnings at annualized rates of 6.8% and 9.8%, respectively, over the last 10 years. Lines are mostly up and parallel except for EPS declines in ’14, ’19, and ’20. PTPM has trended higher over the last 10 years from 11.3% to 16.1% with a last-5-year average of 13.4%. This is significantly higher than peer (stated as CAS.TO, SEE and REYN) and industry averages.

ROE has trended mostly flat since 2014 with a last-5-year average of 23%. Debt-to-Capital has trended lower since 2013 with a last-5-year average of 46.1% (data not available for ’22), which is significantly lower than peer and industry averages. Quick Ratio and Interest Coverage seem acceptable at 1.92 and 11, respectively.

I assume long-term annualized sales growth of 1% based on the following:

- CNN Business projects 3.5% YOY contraction and 1.2% contraction per year for ’23 and ’22-’24, respectively (based on 9 analysts).

- YF projects 3.7% YOY contraction and 0.8% YOY growth for ’23 and ’24, respectively (8 analysts).

- Zacks projects YOY contraction of 4.2% and 0.8% for ’23 and ’24, respectively (4).

- Value Line projects 5.3% growth per year from ’21-’26.

- CFRA projects 1.5% YOY contraction and 0.7% growth per year for ’23 and ’22-’24, respectively.

- M* provides a 2-year growth estimate of 1.1%.

I assume long-term annualized EPS growth of 1% based on the following:

- CNN Business projects 17% YOY contraction and 8.8% contraction per year for ’23 and ’22-’24, respectively (based on 9 analysts) along with 5-year annualized growth of 1%.

- MarketWatch projects annualized contraction of 8.3% and 4.9% for ’22-’24 and ’22-’25, respectively (13 analysts).

- Nasdaq.com projects 0.9% YOY contraction and 0.3% per year growth for ’24 and ’23-’25, respectively (6, 5, and 2 analysts for ’23, ’24, and ’25).

- Seeking Alpha projects 5-year annualized growth of 3%.

- YF projects YOY contraction of 17.3% for ’23 and 5-year annualized contraction of 7.7% (8).

- Zacks projects YOY contraction of 18.2% and 0.9% for ’23 and ’24, respectively, along with 5-year annualized growth of 5% (5).

- Value Line projects annualized growth of 8.4% from ’21-’26.

- CFRA projects 16.8% YOY contraction and 8.3% contraction per year for ’23 and ’22-’24, respectively, along with 3-year annualized growth of 2%.

- M* estimates long-term annualized contraction of 1.6%.

My Forecast High P/E is 14. Over the last 10 years, high P/E has ranged from 14.4 (’13) to 28.7 (upside outlier in ’20) with a last-5-year average (excluding the outlier) of 16.4.

Forecast Low P/E is 8. Over the last decade, low P/E has ranged from 8.5 (’13) to 14.7 (’20) with a last-5-year average of 12.

My Low Stock Price Forecast of $88.10 is default. This is 39% below the last closing price. The low of the last two years is $110.60, but given such dim growth prospects, the Forecast Low P/E seems reasonable.

All this results in an U/D ratio of 0.3, which makes PKG a SELL. The Total Annualized Return computes to 4.7%.

Over the last 10 years, Payout Ratio has ranged from 33.8% (’13) to 69.6% (upside outlier in ’20) with a last-5-year average (excluding the outlier) of 42.5%. I used 34% as a conservative estimate.

Although the current yield (3.4%) is a bright point for this stock, a PAR (using Forecast Average, not High, P/E) of 0.5% is an exclamation point for what is otherwise a depressing stock study. One of BI’s core principles is to buy stock in high-quality growth companies. While PKG has demonstrated consistent historical growth, the outlook for future growth is muddy at best. With the stock up about 17% in just over three months, it’s now far past the BUY zone.

I like to assess margin of safety (MOS) by comparing my inputs with Member Sentiment (MS). Out of 68 studies over the past 90 days, projected sales, projected EPS, Forecast High P/E, and Forecast Low P/E average 5.4%, 6.3%, 17.8, and 11.8. I am dramatically lower on all inputs. Value Line also projects an average annual P/E of 19, which is higher than MS 14.8 and much higher than my 11. I do see a large MOS in this study, but with the wide range of long-term EPS estimates on either side of zero, I also see good reason to be conservative.

MS has a Low Stock Price Forecast of $107.55, which seems reasonable being 20%+ below the last closing price. I just cannot be convinced to raise mine at this time, however [which would increase the U/D ratio]. Seven long-term EPS growth estimates average 1.7%. My forecast is not much lower, and I would not be surprised to see P/E fall to the bottom of its 10-year range given such anemic growth.

*—Publishing in arrears as I’ve been doing one daily stock study while posting only two blogs per week.

Data Type Conversions with the Automated Backtester

Posted by Mark on October 18, 2022 at 06:45 | Last modified: June 22, 2022 08:36I’ve struggled mightily trying to figure out how to handle types for the option data. I think the current solution may be as good as any and today I’m going to discuss how I got to this point.

The data file is .csv with the following [skipping position zero] fields:

- Date (e.g. 17169)

- DTE (e.g. 1081)

- Stock Price (e.g. 2257.83)

- Option Symbol (e.g. SPX 191220P02025000)

- Expiration (e.g. 18250)

- Strike (e.g. 2025)

- Mean Price (e.g. 203.2)

- IV (e.g. 0.209406)

- Delta (e.g. -0.30844)

- Vega (e.g. 13.1856)

- Gamma (e.g. 0.000417)

- Theta (e.g. -0.12758)

For now, I need the following fields as integers (floats for the decimal portion): 1, 2, 5, 6 (3, 7, 8, 9, 12).

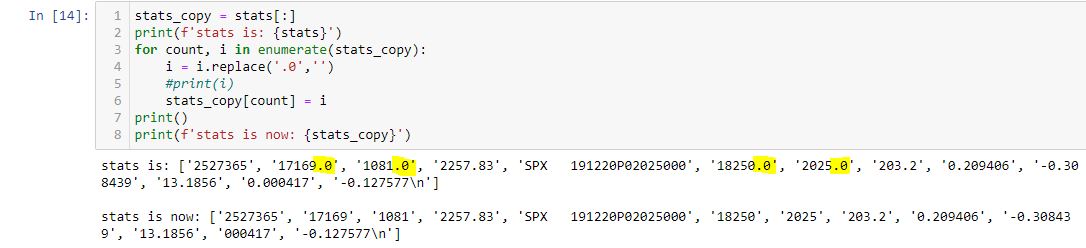

Iterating over the first line of data in the file (skipping the header) with L59 (seen here) yields:

Every field I need as an integer comes up with a .0 at the end. When I try to convert to integer with int(), I get a traceback:

> ValueError: invalid literal for int() with base 10: ‘17169.0’.

I can use int(float())) every time I need to encode data from these columns. I do this 21 times in the program. It may seem like an a lot of unnecessary conversion, but I don’t want to see those trailing zeros in the results file.

If I understood why this happens in the first place, then I might be able to nip it in the bud.

Here’s a short code that works:

Note that each trailing zero (highlighted) is eliminated. This seems like a lot of preprocessing. The fields remain as strings (note the single quotes) and I still have to convert them to integers.

Is all this faster than 21 instances of int(float())?

I mentioned timers a couple times in this post discussing backtester logic. The following is one approach:

import time

start_time = time.time()

elapsed_time_log = open(r”C:\path\timelog.csv”,”a”)

——————-BODY OF PROGRAM——————-

now = datetime.now()

dt_string = now.strftime(“%m/%d/%Y %H:%M:%S”)

end_time = time.time()

elapsed_time = end_time – start_time

comment = ‘v.9′

print(dt_string,’ ‘, elapsed_time,’ ‘, comment, file=elapsed_time_log)

elapsed_time_log.close()

This code snippet appends a line to a .csv file with time and date, elapsed time, and a comment describing any particular details I specify about the current version. This will give me an idea how different tweaks affect program duration.

As a final note, the code screenshot shown above does not work if L1 reads stats_copy = stats because the original list then changes. This gave me fits, and is probably something every Python beginner encounters at least once.

What’s the problem?

With stats_copy = stats, I don’t actually get two lists. The assignment copies the reference to the list rather than the actual list itself. As a result, both stats_copy and stats refer to the same list after the assignment. Changing the copy therefore changes the original as well.

Aside from the slicing implemented in L1, these methods should also work:

- stats_copy = stats.copy()

- stats_copy = list(stats)

-

Categories: Python | Comments (0) | Permalink

NFLX Stock Study (2-2-23)

Posted by Mark on October 13, 2022 at 07:04 | Last modified: July 25, 2023 10:51I recently* did a stock study on Netflix Inc. (NFLX) with a closing price of $361.99.

CFRA writes, “Netflix is the world’s largest Internet subscription service for accessing TV shows and movies.”

This large-sized company has grown sales and earnings at annualized rates of 26.6% and 58.4%, respectively, over the last 10 years. Lines are mostly up and parallel except for EPS declines in ’15 and ’22. PTPM has trended higher over the last 10 years from 3.9% to 16.6% with a last-5-year average of 13.4%. This trails peer (stated as PARA and FOX) and industry averages.

ROE has trended up from 9.2% to 21.6% over the last 10 years with a last-5-year average of 26%. Debt-to-Capital increased from 27.3% in ’13 to 66.4% in ’18 before declining to 40.9% in ’22. The last-5-year average is 56.5%, which is higher than desired. Interest Coverage is somewhat reassuring at 8, but Quick Ratio offers little comfort at 0.96. As of Q2 2022, the M* analyst describes the company “in a decent position” with $14.2B long-term debt and $7.8B cash. Management has stated the firm should not need to tap the credit market in the future to fund its ongoing content spending, but this can always change.

I assume long-term annualized sales growth of 8% based on the following:

- CNN Business projects 8.5% YOY and 10.2% per year for ’23 and ’22-’24, respectively (based on 36 analysts).

- YF projects YOY 8.9% and 11.8% for ’23 and ’24, respectively (32 analysts).

- Zacks projects YOY 8% and 11.6% for ’23 and ’24, respectively (12).

- Value Line projects 9.7% annualized growth from ’21-’26.

- CFRA projects 9.4% YOY and 10.5% per year for ’22 and ’21-’23, respectively.

- M* provides a 2-year estimate of 10.2%.

I assume long-term annualized EPS growth of 8% based on the following:

- CNN Business projects 13.7% YOY and 19.6% per year for ’23 and ’22-’24, respectively (based on 36 analysts), along with 5-year annualized growth of 24%.

- MarketWatch projects 17.8% and 20% per year for ’22-’24 and ’22-’25, respectively (45 analysts).

- Nasdaq.com projects 26.6% and 28.9% per year for ’23-’25 and ’23-’26, respectively (14, 7, and 2 analysts).

- YF projects YOY 14.9% and 26.2% for ’23 and ’24, respectively, along with 16% per year for the next 5 years (32).

- Zacks projects YOY 11.9% and 28.3% for ’23 and ’24, respectively, along with 19.2% per year for the next 5 years (14).

- Seeking Alpha projects 5-year annualized growth of 24.5%.

- Value Line projects 7.7% per year from ’21-’26.

- CFRA projects 16.6% YOY and 21.5% per year for ’22 and ’21-’23 along with 3-year annualized growth of 18%.

- M* gives a long-term estimate of 18.2%.

I’m forecasting near the bottom of the long-term-estimate range (8.9% – 26%). Because a rebound is forecast following a sharp [quarterly] EPS drop in ’22, I decided to override projection from the last annual (vs. quarterly) data point.

My Forecast High P/E is 35. High P/E has come down from 210 in ’13 to 61.3 in ’22 with a last-5-year average trending lower at 93.9. At some point, I expect P/E to fall into a “normal” range.

My Forecast Low P/E is 25. Low P/E has come down from 49.1 in ’13 to 16.4 in ’22. The last-5-year average is trending lower at 48.1. Again, at some point I expect this to fall into a “normal” range and we may already be starting to see this.

My Low Stock Price Forecast of $247.7 is default. This is 31.2% below the last closing price. The 52-week low price is $162.7.

All this results in an U/D ratio of 1.3, which makes NFLX a HOLD. The Total Annualized Return (TAR) is projected at 7.2%.

A PAR (using Forecast Average, not High, P/E) of 3.9% dictates waiting for a lower price. I certainly see room for downside stock volatility as my Low Stock Price Forecast is > 50% above the 52-week low.

If I can glean any current optimism for buying prospects then it would be in the margin of safety, which I can assess through comparison with Member Sentiment (MS). Out of 333 studies over the past 90 days, projected sales, projected EPS, High P/E, and Low P/E average 12.9%, 11.8%, 65.3, and 54.3, respectively. I am lower on all inputs—especially on P/E. Value Line projects a future average annual P/E of 35.5, which is also higher than my 30.

MS has a Low Stock Price Forecast ~$239, which is lower than mine. A closer look reveals some projected lows over $300 (some much higher than the current price) and some under $100. When I exclude these 67 studies, the MS Low Stock Price Forecast drops to $198.69. While that would pull NFLX even farther from the Buy zone in my study, at -31.2% I think my Low Stock Price Forecast is sufficient.

Projected High Price is where my study really diverges from MS: $511 vs. their $1,135.

*—Publishing in arrears as I’ve been doing one daily stock study while posting only two blogs per week.

Backtester Logic (Part 11)

Posted by Mark on October 10, 2022 at 06:45 | Last modified: June 22, 2022 08:35Moving on through the roadmap presented at the end of Part 9, let’s press forward with trade_status.

trade_status operates as a column in btstats to indicate trade progress and as a control flag to direct program flow.

You may have noticed the former by looking closely at the dataframe code snippet from Part 10. In the results file, this describes each line as ‘INCEPTION’, ‘IN_TRADE’, ‘WINNER’, or ‘LOSER’ (also noted in key).

As a control flag, trade_status is best understood with regard to the four branches of program flow (i.e. control_flag). The variable gets initiated as ‘INCEPTION’. This persists until the end of the find_short branch when it gets assigned ‘IN_TRADE’. At this point, the program no longer has to follow entry guidlines but rather match existing options (see third paragraph of Part 2). Once the whole spread has been updated at the end of update_short, the program can evaluate exit criteria to determine if trade_status needs to be assigned ‘WINNER’ or ‘LOSER’. In either of those cases, the trade is over and:

- Variable reset can occur.

- ‘INCEPTION’ gets assigned to trade_status.

- find_long gets assigned to control_flag.

- wait_until_next_day is set to True.

One variable not reset is current_date. This is needed in L65 (see Part 2) along with wait_until_next_day. For completeness, I should probably reset current_date as part of that else block (L68) and assign it once again as part of find_short or in the find_long branch with trade_date in L75.

With regard to exit logic, I have the following after variables are calculated and/or assigned in update_short:

The only exit criteria now programmed are those for max loss and profit target, but this must be expanded. At the very least, I need to exit at a predetermined/customizable DTE or when the short option expires. This may be done by expanding the if-elif block. If the time stop is hit and trade is up (down) money then it’s a ‘WINNER’ (‘LOSER’).

I will also add logic to track overall performance. I can store PnL and DIT for winning and losing trades in separate lists and run calculations. Just above this, I can check for MAE/MFE and store those in lists for later plotting or processing. I can also use btstats. Ultimately, I’d like to calculate statistics as discussed in this blog mini-series. I will take one step at a time.

I conclude with a quick note about data encoding. Following the code snippet shown in Part 1, I have:

![]()

That imports each option quote into a list—any aspect of which can then be accessed or manipulated by proper slicing.

That ends my review of the logic behind a rudimentary, automated backtester. My next steps are to modify the program as discussed, make sure everything works, continue with further development, and to start with the backtesting itself.

As always, stay tuned to this channel for future progress reports!

Categories: Python | Comments (0) | PermalinkAMZN Stock Study (2-1-23)

Posted by Mark on October 7, 2022 at 06:52 | Last modified: February 27, 2023 17:01I recently* did a stock study on Amazon.com Inc. (AMZN) with a closing price of $103.13.

Value Line writes:

> Amazon.com is the largest online retailers [sic]. The company opened

> its virtual doors in 1995. Sales breakdown (2021): North America;

> 59% of sales. International sales, 27% of total. Amazon Web Services

> (AWS), 14%. Third-party sellers (Marketplace) account for about 20%

> of sales. Seasonality: Q4 accounted for 29% of ’21 revenue.

> Acquired Audible.com, ’08, Zappos, ’09, Whole Foods Market, ’17.

This mega-sized (> $50B annual revenue) company has grown sales at an annualized rate of 26.1% over the last 10 years and EPS 71.1% per year since 2016 (excluding previous years with tiny EPS that skew the historical average even higher). Lines are mostly up and parallel except for EPS decline in ’22. PTPM has trended higher over the last 10 years from ~1% to ~8% with a last-5-year average of 5.3%. This slightly trails peer (stated as VIPS, JDD, and PDD) and industry averages.

ROE has trended up from ~0% to ~27% over the last 10 years with a last-5-year average of 22.1%. Debt-to-Capital has increased from 31.9% to 45.7% with a last-5-year average of 49.8%. This is lower than peer and industry averages. Although Interest Coverage is only 5.6 and the Quick Ratio only 0.68, the M* analyst writes:

> The balance sheet is sound with a net cash position and only modest

> gross debt. We expect the balance sheet to remain sound as the

> company has typically maintained a conservative balance sheet and

> generates more than enough FCF from [Amazon Web Services] and

> advertising to fund growth throughout the business.

I assume long-term annualized sales growth of 8% based on the following:

- YF projects YOY 8.6% and 9.6% growth for ’22 and ’23, respectively (based on 46 analysts).

- Zacks projects YOY 8.6% and 9.1% growth for ’22 and ’23, respectively (13).

- Value Line projects 17.8% growth per year from ’21-’26.

- CFRA projects 13.3% YOY and 10.8% per year for ’22 and ’21-’23, respectively.

- M* provides a 2-year estimate of 8.6%.

I assume long-term annualized EPS growth of 9% based on the following:

- CNN Business projects 5-year annualized growth of 12.2%.

- MarketWatch projects annualized ACE of -8.1% and 11.6% for ’21-’23 and ’21-’24, respectively (based on 54 analysts).

- Nasdaq.com projects 65.8% YOY and 66.9% per year for ’24 and ’23-’25, respectively (12, 8, and 4 analysts).

- YF projects YOY growth of -103.7% and 1433% as negative ’22 earnings rebound in ’23 off a fractional base (46).

- YF also gives a 5-year annualized estimate of 26%.

- Zacks similarly projects YOY growth of -104.3% and 1228% as earnings turn negative in ’22 then rebound in ’23 (11).

- Zacks gives a 5-year annualized estimate of 18%.

- Value Line projects annualized growth of 21.2% from ’21-’26.

- CFRA projects -103.7% YOY and -24.6% per year for ’22 and ’21-’23, respectively.

- M* gives a long-term growth estimate of 8.9%.

I’m forecasting near the bottom of the long-term-estimate range (8.9% – 26%). Because a rebound is forecast following a sharp [quarterly] EPS drop in ’22, I decided to override projection from the last annual (vs. quarterly) data point.

My Forecast High P/E is 35. Since 2016, high P/E has eased from 173 to 58.2 (2021). The last 5-year average is 106.1. At some point, I expect P/E to fall into a “normal” range, but predicting when this happens is like taking a shot in the dark.

My Forecast Low P/E is 25. Since 2016, low P/E has eased from 97 to ~44 (2021) with a last 5-year average of 65.3. I expect this to fall into a “normal” range eventually (I’m astounded that this hasn’t happened already to the mega-sized company).

My Low Stock Price Forecast is $81. The default low price is $27.30 based on the depressed $1.09 EPS. This does not seem reasonable. Instead, I will use the 2020 low price of $81.30, which is 21% below the last closing price.

All this results in an U/D ratio of 3.2. This makes AMZN a BUY with a Total Annualized Return (TAR) of 11.1%.

AMZN’s 17% ownership stake in RIVN is what makes this analysis so complex. AMZN lost $10.4B over the first nine months of 2022 due to the drop in RIVN stock price. This is why analysts forecast -100% EPS growth for 2022 and why some 2023 [provided that RIVN shares do not continue the precipitous decline] growth projections are over 1000%. In my view, any math amounting to a 20%+ long-term (e.g. 3-5) EPS growth rate after years 1-2 are negative is suspect.

While TAR is decent, PAR (using forecast average, not high, P/E) is only 7.7%. Is it reasonable to expect the former, which is consistent with the highest long-term analyst estimates?

To answer this, I assess margin of safety (MOS) by comparing my inputs with Member Sentiment (MS). Out of 1142 studies over the past 90 days, projected sales, projected EPS, high P/E, and low P/E average 13.9%, 17%, 78.6, and 67, respectively. I am dramatically lower on all inputs.

To calculate average MS Low Stock Price Forecast, I excluded 199 studies using $100 or more. At least half of these were four digits, and I deem all them to be unreasonable and/or invalid. The revised averages are 13.1%, 16.4%, 73.6, and 61.5, respectively: still well higher than mine. The average Low Stock Price Forecast is $70.50, which is lower than mine and would have resulted in a HOLD for this study rather than BUY. I’m not sure how meaningful this is as I would similarly have had a lower Low Stock Price Forecast had I chosen to use the 2020 low—a decision one could argue to be unreasonable.

While my aim is to use MS to evaluate MOS, I wonder if such comparison here might be apples-to-oranges because I don’t know how many changed projection from the last quarterly (default) to annual data point. Nevertheless, both my growth rate and P/E projections are lower than MS. Even if the conservativism of one set effectively offsets the [more aggressive decision to] override from quarterly to annual data point, I still have the other conservative set providing MOS.

And Value Line has a projected average annual P/E of 40 compared to my 30, which further bolters the conservative case.

Despite the lackluster PAR, given the apparent MOS I like a BUY on these shares up to $104.

*—Publishing in arrears as I’ve been doing one daily stock study while only posting two blogs per week.

Backtester Logic (Part 10)

Posted by Mark on October 4, 2022 at 07:11 | Last modified: June 22, 2022 08:35Today I will continue by following the road map laid out at the end of Part 9.

I will begin with the results file. I have been using Jupyter Notebook for development and I can plot some graphs there, but I want to print detailed results to a .csv file. I am currently generating one such file that shows every day of every trade. Eventually, I want to generate a second file that shows overall trade statistics.

The results file gets opened at the beginning and closed at the end of the program with these lines:

![]()

![]()

In an earlier version, I then printed to this file as part of the find_short and update_short branches with lines like this:

While I find the syntax interesting, I realized these are pretty much just string operations that won’t help me to calculate higher-level trade statistics. Numpy will be much better for that, which is why I decided to compile the results into btstats (dataframe). Done that way, I can still get the results file in the end with this line:

![]()

The dataframe is created near the beginning of the program:

Most of the columns have corresponding variables (see key) and/or are derived through simple arithmetic on those variables.

Now, instead of printing to the results file in two out of the four branches I add a list to the dataframe as a new row:

I searched the internet to find this solution here. One nice thing about Python is that I can find solutions online for most things I’m looking to accomplish. That doesn’t mean I understand how they work, though. For example, I understand df.loc[] to accept labels rather than integer locations (df.iloc[], which I have also learned cannot expand the size of a dataframe). len(btstats.index) is an integer so I’m not sure why it works. This is a big reason why I still consider myself a pupil in Python.

L127 is an example of variable reset (discussed in Part 9). This is what I want to do for every variable once it has served its purpose to make sure I don’t accidentally use old data for current calculations (e.g. next historical date).

Let’s take a closer look at L121:

![]()

The data file includes a date field as “number of days since Jan 1, 1970” format. Multiplying that by 86400 seconds/day yields number of seconds since midnight [UTC], Jan 1, 1970, which is the proper format for the datetime module’s UTC timestamp. I can now use the .strftime() method and ‘%b’ to get the first three letters as an abbreviated month name. Being much more readable than a nonsensical 5-digit integer, this is what I want to see in the results file.

The light at the end of the tunnel is getting brighter!

Categories: Python | Comments (0) | Permalink