STT Backtesting Notes (Part 2)

Posted by Mark on November 29, 2021 at 07:14 | Last modified: July 15, 2021 12:05I continue with miscellaneous observations from recent STT backtesting done in OptionNet Explorer (ONE):

- I did not use PT or max losses, which would require separate tranche monitoring. I realized afterward that I had not separated tranches by trade ID. This is discouraging because as it was, I had difficulty switching between combined/separate isolation modes and [de]selecting position and/or model for adequate visualization to set up trades.

- I used a global bearish STT for adjustment when technicals turned bearish. Per previous bullet point, monitoring separate tranches is important to roll back or exit tranches by the time short/upper strikes are breached.

- My bias is to save money on debit spreads and to buy only when market conditions turn ugly even though I’ll have to pay more at that time. Although I believe the STT may be a profitable strategy, always-on insurance costs extra. Starting without the debit spreads is essentially trading an income STT. Either way, before hanging tight to this bias I really should give the standard STT a chance to see how it fares without loading the additional credit at inception.

- With or without always-on insurance, I still haven’t quantified exactly how profitable the strategy might be.

- I sometimes lost count of STT and tail-hedge tranches. The idea is to sell an STT every time a tail hedge matures. Upon realizing I had gotten behind with tail hedges, I doubled the number of NPs with the intent to sell one fewer STT upon maturation to catch up.

- The last bullet point suggests additional ONE limitations: not showing total count of long/short contracts, not being able to click on a particular expiration and see statistics for just those contracts, and not being able to click a button to jump straight to farthest-dated contract (as I am able to do with to the shortest-dated). I felt like I needed a separate spreadsheet to monitor current number of contracts and total tranches (and trade IDs) for STT and tail hedge.

- I discovered reverse calendar/diagonals taking shape from extra LPs with NPs in far-dated months after closing NTM/losing STTs. Closing NPs for max loss would avoid SOD risk. Alternatively, I could choose to pay some higher price to force tail-hedge maturity and sell a new STT at the same time.

- Tail hedges are always OTM from STTs themselves and I question their lift strength in this ratio (also see Part 1 comments on convexity). As noted in the third paragraph of Part 1, next time I will buy one month closer (perhaps planning to at least close the embedded STT PCS if necessary when associated tail hedges expire).

- What would happen if debit spreads were purchased one month closer?

- I kept an eye on PMR (down 12-14% on the underlying). I should also monitor LEL at trade inception.

- At one point, I clicked ahead to the next day and was surprised to see a blank risk graph. All positions had expired and the previous months had not given opportunity to sell new STT tranches as tail hedges did not mature. This argues for a supplemental volatility-based or episodic STT entry should market conditions turn bearish (although when the market gets crazy, being totally out isn’t a bad thing; see first bullet point in Part 1).

- The strategy is discretionary with many moving parts and I really don’t know what to track. For this reason, I didn’t keep a spreadsheet and don’t have concrete results to present. This doesn’t sit so well with me.

- Although not implemented in this backtest, I did try to model a couple standard 242s and they seemed nowhere close to delta neutral. I used 25-point strikes and I figure this must have been the result of low delta density. I can always tweak strikes as necessary to change NPD as desired.

I will be doing more backtesting, will hopefully sharpen some of the ill-defined points, and will ideally generate some results to share. Things that might help with this include: PT and max losses, guidelines for UEL and delta bias, clear technical criteria, attention paid to unique Trade IDs, and continuous tracking of inventory.

Easier said than done!

Categories: Backtesting | Comments (0) | PermalinkSTT Backtesting Notes (Part 1)

Posted by Mark on November 26, 2021 at 06:51 | Last modified: July 15, 2021 09:49Today I present miscellaneous notes based on observations seen doing manual STT backtesting in OptionNet Explorer (ONE).

I would like to give a disclaimer about level of sophistication. Someone recently looked at my blog and said, “I was completely lost after two sentences.” I have made particular effort in the past to explain things for an audience unfamiliar with trading concepts. I have cut back on this recently. Please realize my primary motivation for blogging is to organize my thoughts and to keep myself on track with my projects. I don’t need basic definitions because I’m immersed in this stuff every day. Should you have particular questions, always feel free to leave comments below or even contact me via website e-mail.

The backtest begins in Nov 2019 in order to be fully loaded for the March 2020 crash. This is primarily an income STT (BWB) backtested as 10 contracts (five tranches). I hedged starting with nakeds that become 40 LPs upon maturation. I sold the STT in the same month; next time, I will look to sell the STT one month farther out.

I tried to use some rudimentary technical analysis to guide whether I should lean positive or negative NPD. I looked at slope of 50-MA along with IV term structure.

If I’m going to trade this live, then I need to be very clear with technical criteria. Even if the criteria alone do not constitute a profitable strategy, they should at least filter out large contrary moves. I then need to make sure to lean directionally rather than letting NPD grow too large (especially in defensive periods where HV is high and big moves would not surprise).

I charged $20/contract to cover transaction fees. This should be sufficient as discussed here. All expiring contracts were BTC at 3:55 PM. This added expense may be considered to offset crash conditions where larger slippage would be expected.

Here are my general impressions:

- When things get crazy, look to peel back or exit because major adjustments moving around lots of contracts in market crash conditions may not be feasible. I totally forgot about this.

- I was usually short convexity although sometimes T+0 bottomed before reversing higher. I thought the idea with the tail hedge was to generally be long convexity, though.

- While I admit I did not add volatility stress to check convexity, never in 2020 did I see a T+0 smile. Neither was this realized when the underlying tanked despite tail hedges profiting handsomely.

- I did not harvest in this study, which could potentially remove risk for some added cost.

I will continue next time.

Categories: Backtesting | Comments (0) | PermalinkReview of Python Courses (Part 34)

Posted by Mark on November 22, 2021 at 07:30 | Last modified: December 22, 2021 09:20In Part 33, I summarized my Datacamp courses 98-100. Today I will continue with the next three.

As a reminder, I introduced you to my recent work learning Python here.

My course #101 was Introduction to Git. GitHub is a website used for collaboration by sharing projects. This course focuses on Git, which is the tool used on GitHub (and some other sites). The course covers:

- What is version control?

- Where does Git store information?

- How can I check the state of a repository?

- How can I tell what has changed?

- What is in a .diff?

- What is the first step in saving changes?

- How can I tell what’s going to be committed?

- How can I edit a file?

- How do I commit changes?

- How can I view a repository’s history?

- How can I view a specific file’s history?

- How do I write a better log message?

- How does Git store information?

- What is a hash?

- How can I view a specific commit?

- What is Git’s equivalent of a relative path?

- How can I see who changed what in a file?

- How can I see what changed between two commits?

- How do I add new files?

- How do I tell Git to ignore certain files?

- How can I remove unwanted files?

- How can I see how Git is configured?

- How can I change my Git configuration?

- How can commit changes selectively?

- How do I re-stage files?

- How can I undo changes to unstaged files?

- How can I undo changes to staged files?

- How do I restore an old version of a file?

- How can I undo all of the changes I have made?

- What is a branch?

- How can I see what branches my repository has?

- How can I view the differences between branches?

- How can I switch from one branch to another?

- How can I create a branch?

- How can I merge two branches?

- What are conflicts?

- How can I merge two branches with conflicts?

- How can I create a brand new repository?

- How can I turn an existing project into a Git repository?

- How can I create a copy of an existing repository?

- How can I find out where a cloned repository originated?

- How can I define remotes?

- How can I pull in changes from a remote repository?

- What happens if I try to pull when I have unsaved changes?

- How can I push my changes to a remote repository?

- What happens if my push conflicts with someone else’s work?

This does it for my review of Datacamp Python courses.

Categories: Python | Comments (0) | PermalinkMy Latest Cover Letter (Part 6)

Posted by Mark on November 18, 2021 at 07:30 | Last modified: July 12, 2021 09:00Through a series of blog posts (Part 1, Part 2, Part 3, and Part 4), I feel I have done a pretty good job of describing what I seek, what I have done, and what I offer to a prospective financial firm. Organizing and putting all this into words has been a herculean effort for me. One thing that remains quite understated is the content presented in this blog.

In Part 5, I started to bring my writing to the fore with a sampling of blog posts.

To say this blog is extensive would be a vast understatement:

- What it Takes to Trade Full Time (2012)

- optionScam.com (2012)

- Walking it Forward with System Validation (Part 1) (2013)

- Is Independent Trading Success Possible? (Part 1) (2013)

- Portfolio Considerations of a Trading Strategy (Part 1) (2014)

- Can We Scientifically Understand the Financial Markets? (Part 1) (2014)

- The Myth of Unusual Option Activity (Part 1) (2015)

- Correlation Confound (Part 1) (2015)

- Israelsen on Diversification (Part 1) (2016)

- Am I Worthy of Self-Promotion? (Part 1) (2016)

- Professional Performance (Part 1) (2017)

- My Take on Asset Managers (2017)

- Incremental Value (Part 1) (2018)

- Automated Backtester Research Plan (Part 1) (2018)

- Testing the Noise (Part 1) (2019)

- Investment Newsletter Scam (2019)

- Black Swan Trading Systems (2020)

- What Percentage of New Traders Fail? (Part 1) (2020)

- An Insider’s View on Jobs in the Financial Industry (Part 1) (2021)

- Debunking the Williams Hedge (Part 1) (2021)

With the exception of time, this blog really is my job interview. Its entirety makes me the most transparent of candidates you will ever see with regard to motivation and any ulterior motives I could possibly have.

The current mini-series is my best attempt thus far to encapsulate everything I am in the domain of finance: trader, backtester, analyst, commentator, writer, defender, and scientist (in any order you well please).

Categories: About Me | Comments (0) | PermalinkTrader Networking, Trading Success? (Part 2)

Posted by Mark on November 16, 2021 at 06:56 | Last modified: July 11, 2021 10:31Part 1 discussed frustration over spotty e-mails when trying to network with other traders. Should consistent, prompt e-mail replies be a prerequisite for trading group candidates, and does effective networking bode well for trader success?

I honestly don’t know how often people check e-mail these days so I did a quick internet search. Reliable statistics are hard to find, but here are some potential answers:

- 40% of people surveyed thought they checked e-mail 6-20 times per day

- 2009 study: 56.4% of people check their e-mail between 0-5 times per day

- About 15 times per day

- 2021 study: 81% check as little as once per day up to continuously (real-time)

How often e-mail should be checked is also unclear. I have seen so-called “experts” recommend:

- Never in the morning

- Every 24 hours

- Five times or less spread throughout the workday

- Three times per day to limit stress

Any of these would be satisfactory for my purposes. I don’t even need a response the same day. Getting a response within 2-3 days is more than sufficient for the purposes of planning a group meeting a couple weeks out in time.

These cursory findings also confirm my frustration over spotty replies. If most people check e-mail so often then why do my leads seem so disconnected? The caveats listed in Part 1 still apply, of course: accidental oversight could be involved.

Switching gears a bit, I think it safe to say that not too many people have substantial success trading the markets. As discussed in the sixth paragraph here, I have had very little success finding other full-time traders. 90% is the oft-quoted failure rate, which I wrote about in this blog mini-series. I also wrote about it here many years ago, and here I discussed one actual study that suggests the failure rate to be even higher.

I had a challenging time organizing this group, which managed to survive for a couple years. We had decent participation across 7-10 members. 3-4 members presented at least the occasional trade while two of us presented frequently. Only one of us (me) was trading full-time.

I have seen many trading meetups struggle to find consistent attendance and subsequently shut down. The AA District Library once refused to advertise an investing program because historically, they found such content to be in low demand.

I wonder about a possible relationship between consistent group attendance and trader success. Might retail traders benefit by coming together to discuss and develop strategy? Might organized trading teams offer accountability benefits? In my humble opinion, AB-SO-LUTE-LY! For various psychological reasons, getting ahead in trading by working alone is very, very difficult.

I would certainly guess those who work together in groups have more success than those who trade on their own. I have discussed benefits of trading groups in the second-to-last paragraph here, the second paragraph here, and here.

One person who responded to my networking e-mail said:

> I’ve been trading for years, more purchase of securities. But started

> with options about 1 year ago, it’s not easy. Everything I seem to select

> goes the opposite direction 😫… I try to do it every day. lol, well

> at least look at it to select something.

Do I think she could be taught to approach this in a more disciplined, systematic way? Yes! Does she have the necessary commitment to learn, practice, and develop? I would have to know her better to answer that.

If you believe that trading groups are correlated with greater success and if trader networking can lead to the creation of trading groups, then trader networking can definitely be correlated with trading success.

Categories: Networking | Comments (0) | PermalinkTrader Networking, Trading Success? (Part 1)

Posted by Mark on November 12, 2021 at 07:15 | Last modified: June 14, 2021 11:10This will be another (e.g. see here, here, and here) post about trader networking. Submitted for your approval is the question of whether effective networking has anything to do with trader success?

To understand where this comes from, I am new to the Sunshine State and trying to network with other traders. My hope is to meet people and possibly further my trading at the very same time. My preference would be to meet as a group.

Our old friend Meetup.com is my primary source for potential leads. I have joined a few trading- and investment-related meetups in the area. Only one has actually had an [online] event thus far. I have messaged a number of people through the site in an effort to reach out.

My opening salvo is rather benign:

> Hi! I am new to the area and looking to network with other traders.

> Let me know if you would like to chat. Thanks!

I think my bio (introduction) is relatively benign as well:

> Full-time, independent option trader looking to network with other

> like-minded individuals. I’m always interested in the possibility

> for collaborative projects.

I’m a friendly guy. I’m pretty easy going. I’m a good listener. I’m interested in your story and what you have to say. Hopefully I check any ego at the door. Let’s talk, shall we? Sure, why not!*

I approach this in an organized fashion so as not to offend anyone or inadvertently cross boundaries. This means keeping track with a networking spreadsheet (at the risk of becoming a “uses-a-spreadsheet-for-everything” person). If anyone tells me “no,” then I certainly do not want to bother them again. If anyone doesn’t answer then it could be a fake account, a spammer, or someone not real. The notification message could have gone to their spam box, though, or it could just be an oversight in which case a follow-up might be advised. It could also be someone not very consistent with e-mails.

E-mail inconsistency is what really makes me wonder. I used to hear people say things like “I’m not very good with e-mail.” Is that still a thing? As the years go by, smartphone technology has progressed where more and more apps have been created for this, that, and everything else. How many people are away from their phones for lengthy periods of time? I have often considered myself lagging behind on technology but even I am connected most of the time now. I rarely go more than several hours between e-mail checks.

Spotty e-mail response is my biggest problem in these initial networking stages and I debate whether this should be a deal-breaker. I’ve said traders are a fickle lot (e.g. see here, here, and here). I will lose interest if I schedule some small group meetings only to see them canceled because a few people call out sick or [even worse] pull a “no call, no show.”

It’s probably a case of “no risk, no reward,” though, and “you don’t know if you never try.” I’m trying!

I will continue next time.

*—This is the image I’m trying to convey along with the desired outcome.

My Latest Cover Letter (Part 5)

Posted by Mark on November 8, 2021 at 07:45 | Last modified: July 12, 2021 07:42I maintain this blog to hold me accountable for work and related projects. It shows good insight into my activities, my trading, and my related thoughts/education over the years. If presented effectively, I think this blog could be my entire job interview.

At the risk of being repetitive, I am going to include an e-mail sent to the CFA institute in March 2021. Earlier this year, I contemplated taking CFA Level 1. I looked at the CFAI website and scrutinized the criteria to earn the charter. One thing I questioned was my work experience since I technically have not worked in the financial industry proper:

—————————————————————

…the reason for my contact is because I know enrolling to prepare and sit for the CFA exams will take a great deal of time, effort, and money. I hope I can pass them all and should that be the case, I would be heartbroken to be denied a charter because the Institute wouldn’t approve my self-employed work experience.

My résumé outlines much of what I have done as a full-time trader since 2008. I have spent many hours watching trading videos online, attending investment and trading Meetups, attending seminars and webinars, participating in online trader forums, and communicating/collaborating with other retail traders. I have also spent many hours backtesting trading strategies and analyzing performance. I have read and taken copious notes on tens of books related to trading and quantitative finance. I log time in a spreadsheet, which totals over 21,000 hours to date. Although I trade only for myself, I have treated this as a full-time job from the very beginning. This is my passion and my business.

In 2009, I created a trading entity (LLC). My tax returns have listed me as “Trader in Securities” for at least the last 10 years.

I led an options trading group from 2013-2016. We had a handful of regular members. It’s very hard to find other full-time retail traders like myself, which is one reason I have given thought to pursuing formal employment in the industry.

I blog about my work and finance-related topics regularly at http://www.optionfanatic.com. What follows is a sampling of over 1,000 total posts I have written since May 2010:

- Can a Retail Trader Succeed at Algorithmic Trading? (Part 1) (2021)

- Attacking the Python (2020)

- Why is Curve Fitting Such a Bad Word (2020)?

- Testing the Randomized OOS (Part 1) (2019)

- The Trader Meetup Dilemma (Part 1) (2018)

- Beware Fraudulent Claims (2016)

- The Southeastern Michigan Trading Collective (2016)

- Weekly Iron Condor Trade #1 (Part 2) (2015)

- Why Options? (Part 1) (2014)

- Weekly Iron Butterfly Backtest (Part 1) (2013)

- Truth in Backtesting (Part 1) (2012)

The blog is not monetized and from what I can tell, it garners little traffic. I maintain the blog to keep me on track with trading and with related thoughts and projects. It’s a way of holding myself accountable for the work that I do.

Thank you for looking into this! Let me know if I can provide anything else.

—————————————————————

I will conclude next time.

Naked Call Backtest (Part 5)

Posted by Mark on November 5, 2021 at 07:12 | Last modified: July 12, 2021 07:57As mentioned previously, increasing position size makes this profitable: not anything about the naked call strategy itself.

Do any research on Martingale betting systems and you will see they are not recommended. I wrote about this here. The smaller I start as a percentage of the total bankroll, the lower probability I will run into a string of consecutive trades long enough to go bust. Make no mistake, though: it most definitely can happen [and since Mr. Market “can remain irrational longer than you can remain solvent,” it probably will].

What are some ways a strategy like this may be viably implemented?

One way is to position size as a fraction of the entire account. I did calculations in Part 4 based on $240K risk. If this is 10% (for example) of my total account, then I can rest easy because at absolute, never-before-seen worst, I lose 10%.

Another way to trade this responsibly might be to overlay on top of a long strategy that offsets naked call (or vertical spread) losses when the market rallies. Keep in mind that calls are NTM compared to equal-delta puts due to vertical skew, which means portfolio margin requirements can grow faster. Trading fewer call than put contracts as net short premium is one way this can make sense; just remember the number of call contracts may increase at least 16-fold.

Implementation of stop-losses is another avenue for the naked call (or vertical spread) strategy. By improving the avg win:avg loss ratio, I can mitigate position size increases. Stops increase number of losses, though, because a trade cannot recover once it has been closed. Backtesting is needed to better understand whether one factor is clearly more likely to prevail.

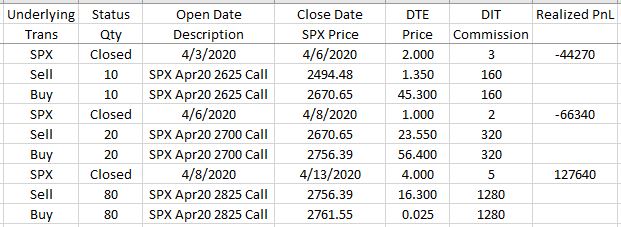

Finally, intraday backtesting (discussed in this blog mini-series) remains undiscovered country. Mine is a once-daily backtest,* which allows up to 24 hours for things to go from bad to worse. The worst backtesting loss is on 4/6/20 when a call sold for $1.35 is closed for $45.30. As mentioned in the second-to-last paragraph here, I think ITM short puts are best rolled before they go OTM. The mirror image dictates rolling short calls before they go ITM. Win percentage would decrease, but magnitude of loss would be lower. Again, backtesting is needed to better understand whether one factor is clearly more likely to prevail.

As discussed in the last paragraph here, by rolling rather than taking on some unknown legging risk and leaving short options to expire worthless, the current backtest errs on the side of conservatism. Rolling involves buying out remaining premium and realizing excessive slippage upon exit, which would both be expected to dampen performance slightly.

* — I used market prices at 3:50 PM until Dec 2020 and at 3:45 PM daily thereafter.

This was due only to inadvertent oversight. The catch-22 is to use data as

close to expiration (4:15 PM ET) while not suffering widened, distorted bid/ask

spreads often seen after normal market close (discussed in fifth paragraph here).

Naked Call Backtest (Part 4)

Posted by Mark on November 2, 2021 at 07:14 | Last modified: July 7, 2021 14:31Do you take it or leave it? I say the latter. With a couple changes, though, this trading strategy becomes a bit more enticing.

All of this exempts previously-addressed caveats having to do with dynamic strategy guidelines:

- Use OptionNet Explorer (ONE) between 3/23/2020 – 7/1/2021.

- Sell 10 naked calls in nearest weekly expiration (1 – 4 DTE) for just over $1.00/contract.

- Assess transaction fee of $16/contract for slippage and commission.

- Monitor market and/or trade once daily at 3:50 PM ET (3:45 PM ET starting Dec 2020).

- If ITM, roll to following weekly expiration as far OTM as possible for credit; increase size with discretion.

- Otherwise, rinse and repeat on expiration day with 10 new contracts.

With regard to (2), the target premium is $1.00 but I aim for ~$1.30 – $1.40 to offset transaction fees. If I have to pay material premium to close (e.g. more than $0.05) then I add to target premium in order to net target premium. For example, if I BTC for $0.75, then I will look to sell the next call for ~$2.00.

With regard to (5), I aim to increase size and leave sufficient cushion in case the market continues upward. What constitutes “sufficient” is what makes this discretionary.

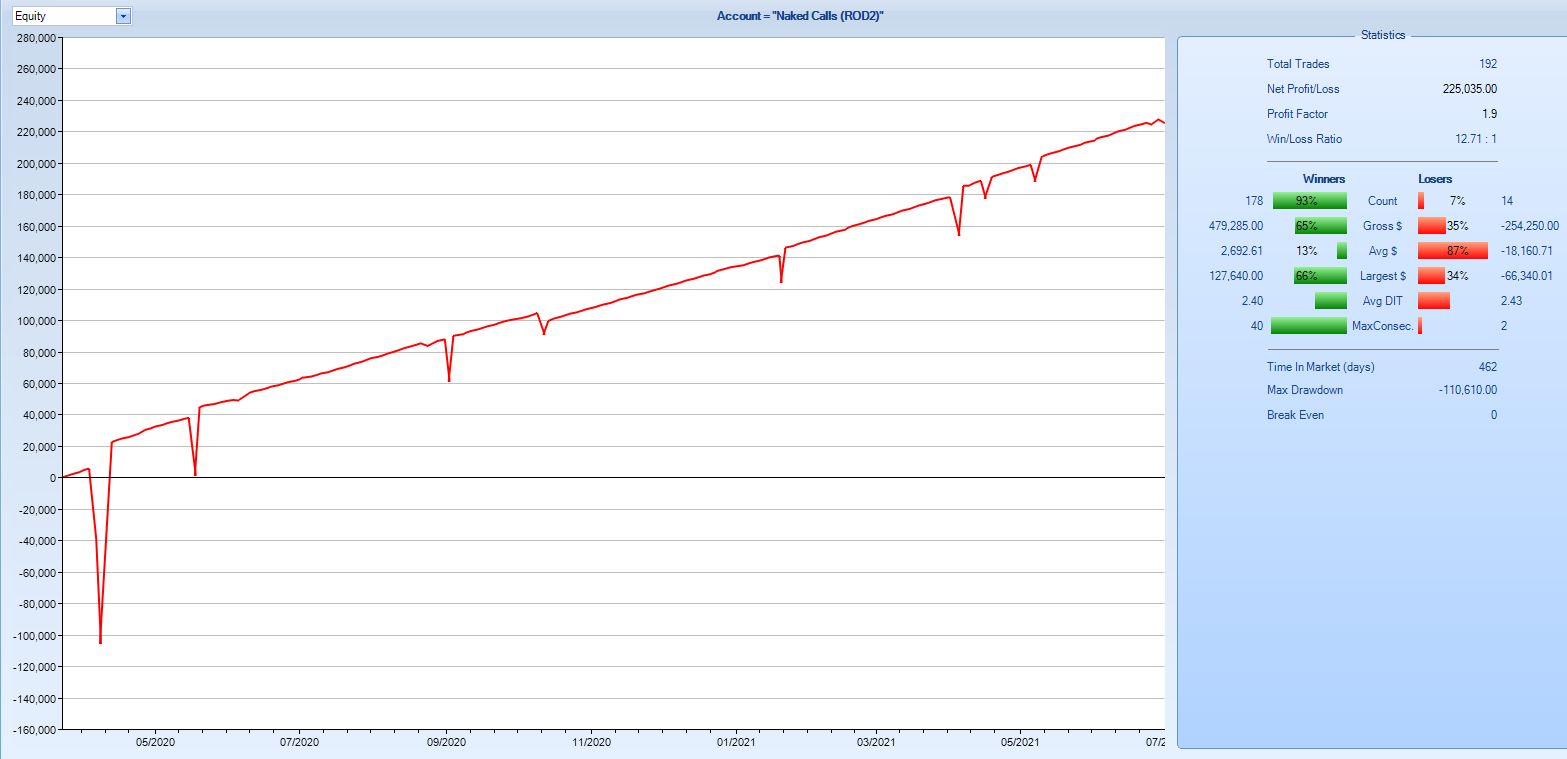

Here are the results:

Shocking improvement from Part 1! This equity curve climbs consistently with eight large, brief pullbacks. The average loss is about seven times the average win. While not so great, the strategy wins 93% of the time.

The maximum drawdown (MDD) occurs here:

Albeit confusing, SPX price increases 10% from April 3 – 14, 2020. I could have rolled the initial 10 to 40 instead of 20, but I would still have lost a second time and had to roll to 80 contracts. A market pullback allows for a profitable exit.

Is this a viable strategy for live-trading? Follow the logic:

- Contract size increases a maximum of eight-fold (significant improvement from 64-fold seen in Part 1).

- Err conservatively by position sizing for a 16-fold increase (one additional consecutive loss).

- Err conservatively by utilizing a 150-point call credit spread that costs an additional dime.

- Account for spread expense by subtracting ($0.10 + $0.16*) x 192 trades from $22,504 backtesting net profit.

- Max margin $15K/contract * 16 contracts = $240K.

- Net profit ~$17,500 in 16 months (rounding up) is ~5.6% annualized return (rounding down).

Given this may supplement a long portfolio, I am somewhat encouraged especially in comparison to the monthly approach.

Unfortunately, increasing position size is what makes this strategy work—not the strategy itself. When I apply constant position size throughout and add the additional cost to spread off risk, I get a profit factor of 1.03: dismal at best.

But, but… I’ll take any bonus return since I’m trading this sufficiently small to support a 16x increase in position size!

Is it conceivable that we could have more than four consecutive big up periods maybe lasting two weeks or more?

Could I go bust as a result?

Yes. Absolutely.

I will continue next time.

* — This is a very conservative estimate; with the option being $0.10, slippage would actually be half that.