[Non]Musings on Vendors

Posted by Mark on April 30, 2020 at 10:16 | Last modified: May 6, 2020 11:53I am not sure exactly what to make of trading system/software vendors, but I believe some understanding of them is essential to long-term trading success.*

Some great discussion about vendors is seen in online trading/investment forums. People debate different angles back and forth. I like to borrow commentary from forums and you have seen this several times. Earlier, I was reviewing a blog idea chock-full of forum excerpts that had 2,800 words. That’s almost an entire month of blogging for me! You probably don’t want to read that much and I don’t really want to type it. I tend to get negative and pessimistic when things start to reek of scam.

I do believe vendors have a place and I think everyone should come to some meaningful understanding on the topic. This isn’t about me getting on my “high horse” and “preaching the gospel.” If I don’t claim to have the answers and if I don’t try to indoctrinate you with them then it’s less work for me aside from being the wrong thing to do.

Today, therefore, I will not try to make a definitive case about vendors one way or another except to say you should know what they are. You should be aware that they exist. You should be able to identify them and I would encourage you to do some thinking on how they fit into the whole landscape of trading and the financial industry. For this reason, I am categorizing this post under “Financial Literacy.”

When I take an inventory of my overall thoughts and feelings, I come up with a few things:

- I know I am an oddity in terms of trading as a business—having replaced my full-time income and surviving eight years and counting: all things for which I am extremely grateful.

- I have a strong suspicion that something is wrong with the financial world.

- I have a strong suspicion many people working Finance do not have a good understanding about how money is made in the markets because they sell what they are told rather than trade.

- I know many trading clichés exist and most times, I can make just as good a case for the converse.

- I have found a great response to 95% of the tweets, posts, and other statements about the markets is “do you have any data to support that?”

- While so many people like to talk about winners, I prefer discussing losers. Talking to people besides myself is probably more enjoyable because they would rather involve celebratory concepts like “financial freedom,” “endless vacation,” “living in Maui,” and “eternal victory.” While these are great marketing anchors to bring people into the game, I am not sure they are reflective of reality.

- When I talk about my losers I sometimes get bitter and angry. While losers aren’t usually pleasant to see, I do believe them to be more important than winners with regard to trading as a whole.

- If I were to teach others then it would be more a scientific approach to the markets and an understanding of the fallacies and buried mines lying in wait than it would be lessons about successful set-ups and claims about how to generate profits. Avoiding losses and generating profits are synthetically equivalent.

The impetus for this post was EZ Color Trading featured on Season 8 of Dragons Den. In the end, only about half of is about vendors. I have therefore edited the title.*

Interestingly, when I browsed over to the EZ Color website, I got “404 Not Found.” This vendor apparently no longer exists.

* — This was originally written in November 2016, but the draft was never completed. Seeing

more recent blog posts (some linked) with overlapping content is very refreshing.

Confirmation Bias

Posted by Mark on April 27, 2020 at 07:38 | Last modified: July 16, 2020 10:18As mentioned in the final sentence, this post from March 2016 begs for a follow-up discussion on confirmation bias.

Just over four years later, here we go!

Confirmation bias is the tendency to interpret new evidence as confirmation of one’s existing beliefs or theories. With regard to finance, this can be a situation where I think I’ve found a viable strategy and [unconsciously] disregard or censor subsequent evidence to the contrary.

In February 2016, I saw a webinar presenting a trading strategy by a guy named Jack. After the presentation, I e-mailed him:

> I totally agree with your premise that if you can generate

> enough income to cover the cost of the long then you

> lose on the trade. Your presentation made it sound

> like you believe this can always be done. What happens

> when it can’t? What is your risk management?

He responded with:

> “What happens when it can’t?”……… haven’t happened

> to me yet…..I’ll let you know when I don’t….lol

> “What is your risk management?”…..Fly has limited loss

> profile……if the market is outside of the fly at expiry

> the loss is what it cost you to place the fly…since the

> fly cost you zero the risk is zero…understand?

>

> Risk on calendar… at expiry WE DO NOT SELL THE LONG

> POSITION we just roll the short position till next week.

> Follow me? If I lose remember it is not money that I’m

> losing… it is only that I have no profits for that cycle.

> Said another way, no money is taken out of my account

> because the market went against me like all other option

> spread positions…this strategy is truly unique…..;)

>

> Hope this helps,

> keep asking.

I responded:

> I think your trading plan is very interesting. However, I

> also think it has a couple fatal flaws. Your presentation

> made it sound like it can’t lose and that’s why I asked

> what happens when it does. Your response suggests you

> still don’t think it can lose because if you lose “it is

> not money that I’m losing.” Every trade can lose. Also,

> there are no “unique” ideas and no Holy Grail exists.

>

> What you presented was not a trading system but rather

> a strategy. If you are trading it, though, then I hope

> you’re trading it more as a system: with defined capital,

> with max loss limits, and with firm understanding how the

> trade can lose and how to recognize when it’s heading in

> that direction. Especially with regard to the latter, if

> you don’t see these things then I strongly believe you

> have more work to do.

>

> Backtesting is a kinder teacher than Live Trading.

>

> I hope I do not seem patronizing or insulting with this

> e-mail. That is truly not my intent. And if I end up

> wrong about this then more power to you.

Why do people feel compelled to defend their strategies or advertise them as if they are infallible and can’t lose?

Confirmation bias is a big reason why. This is another reason I believe trading system development is best done with groups.

Categories: Trader Ego | Comments (0) | PermalinkProprietary Indicators

Posted by Mark on April 24, 2020 at 07:13 | Last modified: April 26, 2020 13:23Proprietary indicators sometimes serve a sketchy purpose in finance.

Check out an article out yesterday (April 23, 2020) on marketwatch.com. The article quotes Sophie Huynh, a Société Générale’s multiasset strategist, who says “investors have likely gotten ahead of themselves… [because] this tech-led recovery… is not sustainable.”

She offers some reasoning to support this prediction. Only in retrospect will we know if she was right or wrong, though, and we will never be able to do anything more than hypothesize as to why.

The article continues:

> Huynh is keeping a close eye on a proprietary indicator that

> tracks positioning of big money managers over a range of

> perceived riskier assets, and so far they are not throwing in

> the towel. “What we’re seeing at the moment is there are no

> signs of capitulation compared to levels seen in 2008, but

> there’s some risk-off that’s settled in,” she said.

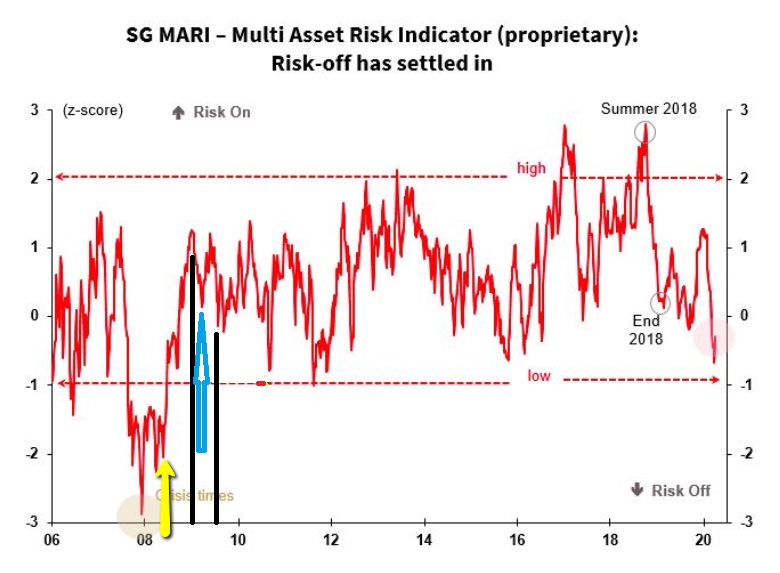

Here’s a chart of the indicator:

At the end of Dec 2007, the indicator bottomed out near -3. I’ll give benefit of the doubt here because the biggest selling occurred in the first couple weeks of 2008 when the indicator had rebounded (albeit to to a still-very-low value).

Because the current indicator (roughly -0.25) is nowhere near the 2008 levels, Huynh is claiming we are not at the bottom.

Can we believe in the indicator, though? Let’s check some values to find out.

The spike lows near the yellow arrow (down to roughly -2.25 and -2.0, respectively) occurred in the first six months of 2008 (around or before 1/4 of the distance between the ’08 and ’10 hashmarks on the x-axis). This seems discrepant because the heavy selling in 2008 came in Q4 (Oct – Nov).

Looking forward, I inserted the black lines to bracket the first half of 2009. This bear market bottomed out with the two weeks ending March 9, 2009. The lowest value of the indicator around that time is highlighted by the blue arrow where it sits in slightly positive territory. That doesn’t seem right.

Moving forward, the period around the Flash Crash (May 2010) is accompanied by a spike down to roughly -0.9. That’s good.

The period around the 2011 summer selloff (US debt downgrade) is accompanied by a spike down to roughly -1. That’s good.

Around August 20-24, 2015, the Brexit selloff is accompanied by a spike down to roughly -0.7.

Around Feb – Mar 2018 when the market corrected over 10%, the indicator looks to be in positive territory. Not good.

Around Oct – Dec 2018 when the market corrected over 10%, the indicator looks to be in positive territory. Not good.

Overall, this indicator is 50/50 based on a small sample size of occurrences in terms of matching up with major “risk off” market declines. A theoretical coin flip would do just as well.

I see many “proprietary indicators” when reading articles in the financial media. I don’t know if such indicators have been accurate in the past (in this case, I was able to do some cursory backtesting). I don’t know if they have been tested for validity. I wouldn’t know what to look for in terms of validity testing—all because they are proprietary (undisclosed). The article is often marketing for some sort of business. In that case, I certainly want to be on the lookout for the fallacy of the well-chosen example (see middle paragraph here).

Red flags fly, for me, whenever I see something labeled proprietary. Too often, this seems to give authors license to write anything convenient.

Categories: optionScam.com | Comments (0) | PermalinkWhat Percentage of New Traders Fail? (Part 3)

Posted by Mark on April 17, 2020 at 12:23 | Last modified: May 16, 2020 15:47Today I continue with excerpts from a Forex website forum discussion in 2013. The initial post, which tries to rebuke traditional wisdom, is Post #1 here. Forum content is unscientific and open to scrutiny. Do your own due diligence and buyer beware.

—————————

• Post #21, Jean:

> The figures don’t show by how much the accounts

> are profitable. Perhaps many are just slightly up in

> % from the start of each quarter, and perhaps all the

> slow and steady growth account holders don’t hang

> out at net forums. Maybe the “95/99% of traders

> lose” is inaccurate and really just a collective

> anger/stressed/disbelief based view of this business

> as so many guys that are both clever and dedicated

> spend years at this and don’t cash in, but spend

> a lot of time together on forums and collectively

> agree on a 95-99% figure…?

• Post #22, Slim:

> Those statistics don’t really mean much as far as

> I’m concerned. Certainly, there will be a lot of

> traders who jump in for three or four months and

> quit. That significantly reduces the “success rate”.

>

> Trading is a profession (think doctor or lawyer).

> You don’t have to go to college to be a good trader

> but you’ll get your “trading degree” one way or

> another [with tuition paid to the market].

>

> Most professionals spend years learning their

> profession. What would be the success rate of a

> surgeon after 4 months of learning? Some can

> probably be a good trader in far less time than

> it takes to be a surgeon but the idea is the same.

>

> Individual retail traders have the added burden

> of becoming entrepreneurs—like an attorney going

> into private practice rather than working for a firm.

>

> I would imagine that the success rate for traders

> who take the time to learn and decide to stick with

> it isn’t so different as the success rate for other

> businesses: ~18 – 20%. You really can’t judge the

> success/failure rate solely by the stats required

> by the CFTC.

• Post #28, Dye:

> Yet more and more people are still buying into this

> long held rumor?? based on what facts? I would like

> to see some stats other than broker numbers that

> can be manipulated just like the price. With a

> market that is so random how can we have such a

> firm number of losers to winners.

• Post #29, Cold:

> It makes no sense and I don’t buy it at all. Maybe

> not 99% but more than 70%. I’ve been in the business

> since 2003 and I can confirm from my own experience.

• Post #30, Slim:

> The fact is, PEOPLE WILL BELIEVE WHAT THEY WANT

> TO BELIEVE regardless of whether there’s anything to

> substantially support the belief.

>

> I think I would have to agree with Cold: more than

> 70% fail. However, I would like to know the success

> rate of those who have toughed it out for at least

> 3 years. I can only guess that the success rate gets

> a little better.

I wonder what Cold and Slim would think about the Brazilian day trading study?

To be continued…

Categories: Financial Literacy | Comments (0) | PermalinkWhat Percentage of New Traders Fail? (Part 2)

Posted by Mark on April 14, 2020 at 11:20 | Last modified: May 16, 2020 15:15Today I continue with excerpts from a 2013 Forex website forum discussion. The initial post (#1), which tries to rebuke traditional wisdom, is seen here.

Forum content is never scientific and always open to scrutiny. Do your own due diligence and buyer beware.

—————————

• Post #6, Raz:

> Even if 99% isn’t accurate (let’s say it’s actually 90%:

> doubtful though) I believe it’s better for a newbie

> to hear the number 99%. Those who can make it

> already know they are in the 1%, and for the others I

> believe it’s good for them to realize Forex is not a

> sure thing and not to quit their day job over.

>

> Of course scammers like you would like people to

> believe they can make 9000$/day (NO EXPERIENCE,

> NO WORK REQUIRED, right?) but that’s just not true.

>

> I’m sick of Forex ads that say “Hi, i’m Rosie and a

> week ago I used to clean toilets… but then I found out

> about Forex. Now I drive a Ferrari! You can do it too!

> Quit your job, sell your house, fill your account and

> sooner then you know it you’ll be a billionaire too!”

>

> It’s a disgrace for brokers and for traders: makes it

> all seem like a scam.

Enter mention of scam. This is commonly seen in forum posts and often discussed on my blog as well. The possibility is out there and the likelihood exists: people just choose to ignore it.

• Post #7, Bab:

> It’s said that failure is not when you fall per se.

> Failure is when you fall and fail to get up again.

> The perception that 90% of traders failed is that

> they blew up but did not rise again or did not “try,

> try, till you succeed.” The 10% successful are those

> who rose after falling. They might have fallen many

> times and learned valuable lessons each time to move

> forward. Failure is experience that can lead to

> success. The brokers figures, if true, might portray

> active traders with a huge amount that have not

> gotten up and therefore gone inactive. This might

> further dilute the successful in a ratio of 1:9.

>

> If these figures are depressing to the new trader,

> then make use of demo accounts to fail virtually.

> Read, learn, understand, and practice for days,

> months, or years on the DEMO. Get experienced and

> succeed with your strategy on DEMO. Eventually, go

> live in small steps, risk only what you can afford

> to lose, and apply strict money management. You

> too can be an elite success.

>

> Good Luck to all who pursue this trading endeavor

> and to those who have almost reached success.

I think there are some good recommendations here.

• Post #8, prak:

> From what I understand the % winning is based on

> balance increase over the quarter. As Oanda pays

> interest on accounts, any account sitting there

> doing nothing went up and therefore is profitable.

>

> The results do not show the trader that makes

> money in one quarter but then blows up the next.

> Just because 20% made money in one quarter does

> not mean any are profitable overall.

• Post #9, jean:

> If any of you are wondering about the NFA retail

> broker client profitability calculation, instead

> of guessing just read this.

>

> After consultation with CFTC staff, NFA provides

> the following information:

>

> “The calculation, including determining the total

> number of non-discretionary retail forex customer

> accounts maintained by the RFED and FCM that

> quarter (Q), should include only accounts that

> executed trades during the Q and/or had an open

> position at any time during the Q. Accounts without

> trades or open positions during the Q should not be

> included in the calculation regardless of whether

> the account maintained a cash balance and/or was

> paid interest or charged any fees during the Q.”

• Post #18, Ekl:

> It will be interesting to see the profitability with

> the filter of at least one trade during the Q. I

> would suspect many accounts are profitable on

> account of accrued interest and not winning trades.

To be continued…

Categories: Financial Literacy | Comments (0) | PermalinkWhat Percentage of New Traders Fail? (Part 1)

Posted by Mark on April 9, 2020 at 10:44 | Last modified: May 16, 2020 15:17I have been interested in the title topic ever since I started trading. I recently stumbled upon an academic paper that analyzed futures day trading in Brazil. The results were fascinating.

What follows are excerpts from a forum discussion I found on a Forex website back in 2013. Forum content is never scientific and always open to scrutiny. Do your own due diligence and buyer beware.

—————————

Here is the initial post:

• Post #1, Wpr:

> Often, I hear mentionined how 95% – 99% of all new

> traders fail. This type of misinformed information

> in my opinion is very misleading and damaging to the

> psyche of those trying to learn how to trade forex.

>

> First the facts.

>

> Brokers inside the USA are now required by the CFTC

> to release the percentage profitability rates along

> with the number of active traders. While the

> following numbers focus on USA, traders worldwide

> should be the same.

>

> The true percentage of profitable traders

> • Oanda has ~50,000 active traders

> • IBFX has 18,579 active traders

> • FXCM has 15,023 active traders

> • Gain has 11,344 active traders

> • GFT has 10,358 active traders

>

> 51% of Oanda traders were profitable in Q3. Others

> are far lower: GFT at 33% and the rest 21% – 29%.

>

> These numbers destroy the myth that 95% – 99% of

> traders are not profitable.

>

> Why this matters to those trying to learn to trade:

>

> If you are told ahead of time that your odds of

> success are extremely rare (knowing that you are

> competing against some of the brightest minds in

> the world), your chances of success are greatly

> diminished compared to if you believed that others

> have succeeded and that you can too.

>

> You can become a profitable trader. A large

> percentage of others have proven it and are doing

> it on a quarterly basis. Believe in yourself:

> many before you have done this and you can too.

>

> Collectively, let’s change the consciousness to a

> positive light enabling more to succeed.

>

> Your thoughts and opinions are welcomed friends.

• Post #2, Fnuts:

> For starters, what metrics do these brokers use to

> rate profitability? What specs? What accounts? Mere

> % is not going to convince anyone here. And

> profitable forex trading takes time and a lot of

> effort on the part of a trader, it’s not slam dunk as

> you make it sound..

>

> Either way, seeing how brokers tend to fudge details

> and have been doing so for some time now, not going

> to trust any % cruncher the brokers may have set up…

• Post #3, XTr

> Were Q1, Q2, and Q4 profitable?

>

> 50% is a breakeven number. You are also getting this

> info from the party itself not an outside source.

>

> Maybe not 95%, but yes 90% of new FX traders FAIL.

>

> FACTS:

>

> 1. Not enough experience trading live money

> 2. Undercapitalization

> 3. Over-leveraging

> 4. Overtrading

> 5. Shady broker practices

> 6. Insufficient understanding of markets let alone FX

> 7. No detachment from emotion and money

>

> Ask any experienced trader on this forum if they have

> HONESTLY ever blown up an early account and the answer,

> nine times out of 10, will be YES.

>

> What makes you think that these “profitable traders”

> aren’t just dumping more and more money into their

> accounts after losing?

To be continued…

Categories: Financial Literacy | Comments (0) | PermalinkTrading System Development 101 (Appendix B)

Posted by Mark on April 6, 2020 at 06:51 | Last modified: May 15, 2020 14:46This year, I have been trying to get more organized by completing rough drafts into finished blog posts. Sometimes I don’t even understand what I have written because it has been so long, but I am presenting them anyway on the off chance someone out there can possibly benefit. In that vein, here are the last loose ends and notes regarding my mini-series Trading System Development 101 (concluded here).

—————————

From the last paragraph here, I could also look at what percentage of iterations are profitable when grouped by VIX cutoff value. I could then know how often a VIX filter would actually work and whether I get those desirable high plateau regions.

This post had a footnote where I indicated some further explanation could be useful. Looking back to that final full paragraph, imagine one set of trendlines might result in X, Y, and Z trades being taken. Were the chart to begin a couple bars later, imagine a different set of trendlines could result in A, B, and C trades being taken. Granted, multiple trendlines generated due to the allowable margin of error are better than zero or few trades (sample size too small). Both sets of trades are equally feasible, though, and should therefore be considered even though multiple open positions are not allowed in backtesting. Timing luck applies here to the trades themselves, as well as the trendlines with respect to where the chart begins and what bars will be available from which to construct trendlines.

The last loose thread I wish to tackle is from the final paragraph here: why is KD’s most common response to me “there is no right or wrong answer?”

This is an example of a standard response I get:

> It could be hurting, hard to say for sure. Try aiming

> for 100-200… a few times and see what happens. Or

> even try 1000 or more. There are some who usually do

> 10 or less, some that keep it under 100, and some that

> always have thousands. So, there is no set answer to

> this, because all can work (and all sometimes don’t).

This almost sounds like Yogi Berra wisdom!

My response is:

> You say there’s no correct answer, but it may be an

> empirical question. You could track the lifetime of

> viable strategies (how long until they break). You

> could then look at strategies with few and compare to

> strategies with lots. Track how long until they break.

> Compare the two groups to see which is longer.

He certainly could do this and I think it would be quite insightful.

However, recall his business model I detailed in the second paragraph here. Anything tested by others are strategies he doesn’t have to test himself. He will never know what everyone tests, but the more strategies tested by others, the more viable strategies will be passed to him. The more diversity in strategies tested by others, too, the more noncorrelation he can realize. The last thing he’d want to receive are strategies similar in one or more ways.

Discouragement of any kind is therefore not in his best interest. Whether it has few or many iterations, optimizes over this or that range, uses this time frame or that one, is mean-reverting or trend-following, etc., as long as it passes his criteria, it’s a strategy he will be very eager to check and/or implement for himself.

Categories: System Development | Comments (0) | PermalinkTrading System Development 101 (Appendix A)

Posted by Mark on April 3, 2020 at 10:42 | Last modified: May 15, 2020 14:14This year, I’ve been trying to get more organized by turning rough drafts into finished blog posts. Sometimes, I don’t even understand what I have written [long ago] in the drafts, but I am presenting them anyway on the off chance that someone out there can benefit. In that vein, I have a number of loose ends and notes regarding my mini-series Trading System Development 101 (concluded here) and related posts that will occupy two further entries.

—————————

When choosing fitness functions, we need to understand how they can possibly deceive. For example, a profit factor of 2.0 may be $5,000 (if it makes $10K and loses $5K) or $50,000 (if it makes $100K and loses $50K). Also, average trade is not per day; $1,000 for a trade held for five days is more attractive than 50 or 500 days.

With regard to my brief experience thus far testing algorithmic strategies, I’m shocked to discover almost nothing works! This is despite all those books with chapters on indicators, all the instructional webinars, and all the educational programs alleging to teach technical analysis. Hardly anything that claims to work is backed by supporting data, either.

With the exception of equities, I have gotten the impression that money is much easier lost than gained. Making money in non-equity markets seems to require a behemoth effort.* With equities, almost everything makes money when bought. Problematic are the occasional sudden, fast, hard corrections and bear markets that wipe out much of the gains in a short period of time. This is no big deal for long-term investors who don’t often look at the market and hold positions for years. For traders who try to profit consistently over the shorter term, this can pose major psychological challenges.

To reiterate a point made near the end of this post, finding a viable trading strategy is probably not about reading an article or chapter on a TA indicator and using it as prescribed. The answer is not to attend an online webinar and implement said strategy verbatim in my live account. Most things I will test will not work; it’s not nearly as easy as the presenters make it sound. The most important thing is a well-thought-out development process and boatloads of patience and motivation.

Going back to this blog mini-series, here’s a note on over-optimization (i.e. overfitting):

> Though not specific to automated trading systems, traders

> who employ backtesting techniques can create systems that

> look great on paper and perform terribly in a live market.

> Over-optimization refers to excessive curve fitting that

> produces a trading plan unreliable in live trading. It is

> possible, for example, to tweak a strategy to achieve

> exceptional results on the historical data on which it was

> tested. Traders sometimes incorrectly assume a trading

> plan should have close to 100% profitable trades or

> should never experience a drawdown to be a viable plan.

> As such, parameters can be adjusted to create a “near

> perfect” plan — that completely fails as soon as it is

> applied to a live market.

I will conclude next time.

* — Most of my testing thus far has been of symmetric strategies: opposite rules for buy and sell short.